VAT (Value Added Tax) is an indirect tax that is paid on goods and services at every level of production and distribution, depending on the value added. It is collected and paid to the government by the businesses. The end consumer is responsible for the resultant cost through the purchase price.

VAT was introduced in the mid-20th century as a more effective substitute for cumulative sales taxes. It was initially staged in France in 1954, with a direction by Maurice Lauré. The system became available to the EEC (European Economic Community) nations in the 1960s and 1970s. VAT is presently utilised around the globe as a standard type of consumption tax.

To register for VAT, a business must apply to its national tax authority, usually online, once its taxable turnover exceeds the legal threshold or voluntarily if beneficial. The process involves submitting business details, bank information, and expected turnover. The business receives a VAT number after approval. It then must charge, collect, and report VAT on taxable sales.

What is VAT (Value Added Tax)?

VAT stands for Value Added Tax, which is an indirect consumption tax. This tax is levied on the value added to goods and services at every step of their production and distribution, from getting the raw materials to selling them to the end consumer. VAT in the UK is a tax added to most products and services sold by VAT-registered businesses. Businesses have to register for VAT if their VAT taxable turnover is more than £90,000.

What Does VAT Stand For?

VAT stands for Value Added Tax. VAT tax means businesses collect it, but the final consumer is the one who is responsible for the cost. It is not a tariff. More than 140 countries worldwide use VAT as an important source of government revenue, which makes it one of the most widely adopted tax systems globally.

What is the History of VAT?

VAT is a recent tax that was initially suggested by Wilhelm von Siemens, a German industrialist, in the early 20th century. He proposed this tax to resolve the issue of accumulating taxes, where each production step taxed the same good multiple times. These accumulating taxes increasingly and unnecessarily inflate the costs to consumers. The modern VAT finally came into existence when Maurice Lauré of the French tax collection agency introduced it on 10 April 1954. The modern tax replaced the older turnover tax with a more equitable and effective system.

The 1957 Treaty of Rome brought VAT to the global stage by requiring member states to implement a common taxation system. VAT was introduced in the UK on 1 April 1973, when it became a member of the EEC (European Economic Community), replacing its purchase tax. 48 countries had adopted VAT by 1989, and it has spread down to the 1990s and 2000s, even to Eastern Europe, following the collapse of communism. Today, 175 out of 193 member states of the UN are using VAT, and this has solidified its position as the most popular tax regime in modern history.

How Does Value-Added Tax Work in the UK?

Value-Added Tax is charged at each stage of the supply chain, from production to the final sale. A manufacturer pays VAT on raw materials and charges VAT when selling to a wholesaler, reclaiming what they paid as input tax. The wholesaler does the same when selling to a retailer. The retailer then charges VAT to the final consumer, who pays it in full and cannot reclaim it. VAT-registered businesses report the difference between VAT charged and VAT paid to HMRC (His Majesty’s Revenue and Customs) every three months.

✓ Free initial consultation

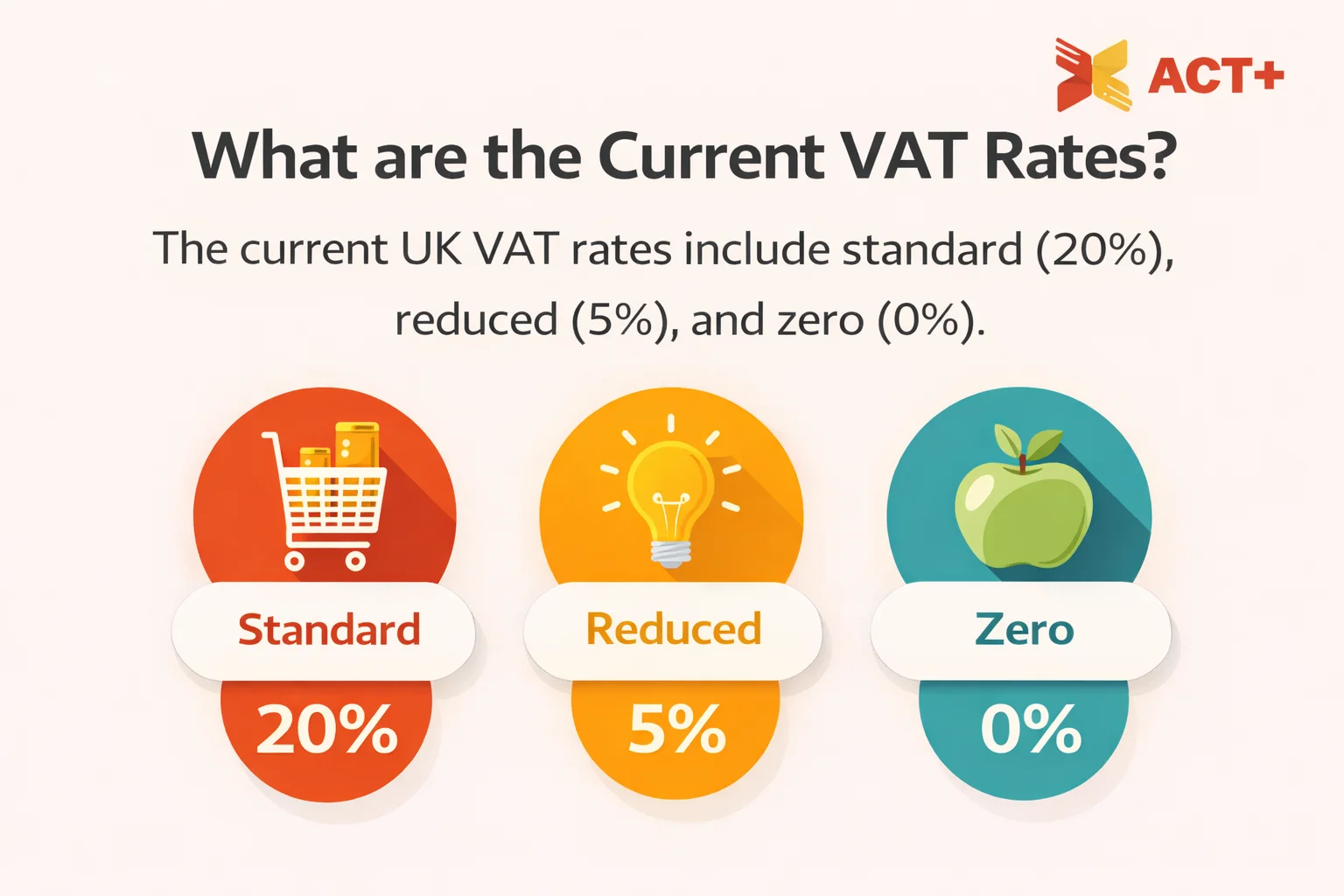

What are the Current VAT Rates?

The current UK VAT rates include standard (20%), reduced (5%), and zero (0%). The applicable rate depends on the goods or services provided. The standard VAT rate of 20% applies to the vast majority of goods and services in the United Kingdom. The 20% standard rate applies to any item or service that does not fall into the reduced or zero-rated categories. The standard rate of VAT covers electronics, furniture, clothing (except children’s), alcohol, restaurant meals, professional services, vehicles, and the vast majority of retail goods.

A reduced rate of 5% covers essential items like domestic energy and children’s car seats. This rate applies to some goods and services where the government wants to offer lower costs to the public, often for health, safety, or environmental reasons. Zero-rated goods and services are still taxable, but the VAT rate is 0%. Businesses must still record these sales and include them in their VAT returns. The benefit is that they can reclaim VAT on related costs and purchases. Zero-rated items include most food, books, and children’s clothing.

VAT-exempt items are not taxed at all, and businesses providing only exempt goods or services cannot reclaim VAT on their expenses. Sectors such as healthcare, education, and financial services remain VAT-exempt. The VAT registration threshold in 2026 remains at £90,000. Businesses must register for VAT once their taxable turnover exceeds £90,000 over 12 months.

What is the History of UK VAT Rates?

VAT was introduced in the UK on 1 April 1973 at a standard rate of 10%, with food, fuel, and housing exempted. Labour cut it to 8% in 1974, while Thatcher raised it to 15% in 1979. It climbed to 17.5% through the 1990s, briefly dropped to 15% during the 2008 financial crisis, and has stood at 20% since 2011.

What are the VAT rates on Different Goods and Services in the UK?

Most goods and services are charged at the standard rate of 20%, unless they are classed as reduced or zero-rated. The reduced rate of 5% applies to items such as home energy and children’s car seats, while the zero rate of 0% covers essentials like most food, books, and children’s clothing. Some goods and services, such as healthcare and education, are fully exempt from VAT.

What does VAT exemption mean?

VAT exemption means VAT-exempt items are not taxed at all. Businesses providing only exempt goods or services cannot reclaim VAT on their expenses. This differs from zero-rated supplies, where VAT is charged at 0%, and businesses can still reclaim input VAT on related costs. Exempt supplies are entirely outside the VAT system. Common examples include healthcare, education, and financial services.

What is VAT in Britain?

VAT in Britain replaced Purchase Tax, and is the third-largest source of government revenue, after income tax and National Insurance. It is administered and collected by HM Revenue and Customs, primarily through the Value Added Tax Act 1994. VAT is a tax added to most products and services sold by VAT-registered businesses, with businesses required to register once their taxable turnover exceeds £90,000. VAT is an indirect tax because the tax is paid to the government by the seller rather than the person who ultimately bears the economic burden of the tax, the consumer.

When Did VAT Start in the UK?

VAT started in the UK on 1 January 1973, when the UK joined the European Economic Community. Value Added Tax replaced Purchase Tax on 1 April 1973. Value-Added tax in the UK was introduced at a standard Value-Added tax rate of 10%, applied to most goods and services across England and the wider UK.

What is the Value Added Tax Number?

A Value Added Tax Number is a unique identifier issued by HMRC to VAT-registered businesses in the UK for tax records and payment purposes. It is also referred to as a VRN (VAT Registration Number). UK VAT numbers follow a specific structure and consist of nine digits. The number starts with the prefix “GB”, for example, GB123456789. The first two letters represent the country, while the following numbers are unique to the business.

Businesses in the UK with a turnover of over £90,000 are legally required to register for VAT and are issued a VAT Registration Number. Companies can also voluntarily register for a VRN. A VAT number is used to track and report VAT obligations to HMRC. It is used when issuing invoices to clients, filing VAT returns with HMRC, and when claiming VAT back on goods or services purchased for the business. It is also necessary for customers and suppliers to verify VAT status.

The UK GOV service is used to check if a UK VAT registration number is valid. It is also used to find the name and address of the business the number is registered to. The VAT numbers for most businesses and organisations are found on their invoices, receipts, or websites.

✓ Free initial consultation

How to Register for VAT?

To register for VAT, sign in using a Government Gateway ID on the HMRC website. A new account is created at that stage if one does not already exist. Navigate to “Get another tax, duty or scheme” once logged in and select VAT. Business details are then filled in as prompted through the steps in the portal.

HMRC usually processes applications within 10 working days, and a VAT certificate is received within 30 days. This certificate includes the unique VAT number and confirms when to submit the first VAT return and make the first payment. Businesses need to provide legal business information when submitting a VAT application online through the Government Gateway.

Add VAT to all goods and services sold unless they are zero-rated or exempt once HMRC approves the application. All VAT-registered businesses must use Making Tax Digital-compatible software to record transactions and submit VAT returns to HMRC regularly.

What Is the VAT Threshold in the UK?

The VAT threshold in the UK is currently set at £90,000. A business must register for VAT if its taxable turnover exceeds £90,000 in the last 12 months or is expected to exceed this amount in the next 30 days. Businesses based outside the UK that supply any goods or services to the UK must register, regardless of their turnover.

The deregistration threshold remains at £88,000. It means businesses whose taxable turnover falls below this figure can usually apply to cancel their VAT registration. Voluntary registration is also an option for businesses whose turnover is below the £90,000 threshold.

How to Calculate VAT UK?

To calculate VAT in the UK, the basic formula is to add VAT and multiply the net price by (1 + VAT rate). Divide the gross price by (1 + VAT rate) to remove VAT.

- Adding VAT to prices: Gross = Net × (1 + VAT rate)

- Removing VAT from prices: Net = Gross ÷ (1 + VAT rate)

A net price of £500 × 1.20 = £600 gross price, including VAT, with £100 being the VAT amount at the standard 20% rate. Removing VAT from a gross price requires dividing by 1.20. So £600 ÷ 1.20 = £500 net. A common mistake is subtracting 20% instead of dividing, as £600 minus 20% gives £480, which is incorrect. Simply replace 1.20 with 1.05 in the same formula for the reduced rate of 5%.

How Does Value-Added Tax Work For Business?

VAT is collected at each stage along the supply chain and charged on the value added to goods and services at each stage of production and distribution. VAT-registered businesses can deduct the VAT they have paid to other businesses from the VAT they have collected. This deduction confirms that the tax is neutral for businesses that make onward taxable supplies, regardless of how many transactions are involved.

Include VAT in the price of all goods and services at the correct rate, with records kept of how much VAT is paid on business purchases. The amount of VAT charged to customers and paid to other businesses must be reported to HMRC by sending a VAT Return, usually every three months. The difference is owed to HMRC if more VAT has been charged than paid. HMRC will usually repay the difference if more VAT has been paid than charged.

What Does “Inclusive of VAT” Mean?

Inclusive of VAT means the Value Added Tax is already built into the total amount shown, with no extra charges added at the end. What is seen is paid for. This is the standard pricing method for B2C (Business-to-Consumer) transactions where simplicity and transparency really matter. Showing prices inclusive of VAT is not only good practice but also a legal requirement in the UK. This requirement makes sure the price seen is the price paid with no surprises at checkout.

VAT-inclusive prices already have the appropriate sales tax, which makes it easier for customers to make a purchase. For example, a product priced at £120 VAT inclusive means the net price is £100, and VAT is £20.

What is the difference between VAT and Tax?

The factors that differentiate between VAT and Tax are the collection method, responsibility, point of collection, reclaimability, transactional nature, and transparency.

The difference between VAT and Tax is mentioned below.

- Collection method: VAT is an indirect tax because individuals do not pay it directly to the government. Suppliers act as intermediaries by collecting the VAT from customers at the point of sale and remitting it to the government. Tax, however, is paid directly to the government by an individual or organisation based on their income or profits.

- Responsibility: Every business along the value chain receives a tax credit for the VAT already paid. The end consumer does not receive this credit, which makes VAT a tax on final consumption. The burden for (direct) tax is entirely on the person or business earning the income.

- Point of collection: VAT is assessed on the value added at each production stage of a good or service. Tax is collected once, based on income or profits earned over a set period, rather than at multiple points throughout the supply chain.

- Reclaimability: VAT deductions are only available to businesses, not final consumers. This system makes sure that VAT is only applied once, at the final point of sale, preventing the tax from being charged multiple times along the supply chain. Direct taxes offer no equivalent reclaim system.

- Transactional nature: VAT is more transactional in nature. It means VAT is imposed at every stage of the supply chain, from production to the final sale of goods or services. Direct taxes are based on income and are only imposed on individuals or entities that meet some income thresholds.

- Transparency: VAT is more transparent and effective than traditional sales tax. Value-Added Tax is applied uniformly at each stage of production and distribution, which makes it easier to administer and collect. Tax is based on declarations of income or profit, which is more difficult for governments to verify and enforce.

✓ Free initial consultation

What is the difference between VAT and GST?

VAT (Value Added Tax) is a consumption tax mainly on goods, applied at each stage of production where value is added, often with differing state-level rates. GST (Goods and Services Tax) is a broader, unified tax covering both goods and services. GST replaces multiple indirect taxes and reduces the accumulating (“tax on tax”) effects.

What is the difference between VAT and sales tax?

VAT (Value Added Tax) is a multi-stage consumption tax applied at each step of production and distribution, where tax is charged only on the value added at each stage. Sales tax, however, is a single-stage tax applied only at the final sale to the consumer. VAT is collected throughout the supply chain, but sales tax is collected once at purchase.

What is the difference between a direct tax and an indirect tax in VAT?

Direct tax is paid directly by an individual or business to the government and cannot be transferred, like income tax. Indirect tax, like VAT, is applied to goods and services and can be passed on to consumers through prices. VAT is an indirect tax, where the final burden falls on the end consumer, not the seller.

What is the difference between input VAT and output VAT?

Input VAT is the tax a business pays on goods and services it purchases for operations, whereas output VAT is the tax it charges customers on sales. Businesses usually reclaim input VAT but must remit output VAT to the government. The difference between output VAT and input VAT determines whether the business owes tax or receives a refund.

What are the different types of VAT schemes?

The different types of VAT schemes are Standard VAT Accounting, VAT Flat Rate Scheme, VAT Cash Accounting Scheme, VAT Annual Accounting Scheme, VAT Retail Schemes, and VAT Margin Scheme.

The different types of VAT schemes are outlined below.

- Standard VAT Accounting: The Standard VAT Accounting Scheme requires businesses to charge VAT on sales, reclaim VAT on purchases, and submit regular VAT returns to HMRC, usually quarterly.

- VAT Flat Rate Scheme: Businesses pay HMRC a fixed percentage of their gross turnover based on their industry type, rather than calculating VAT on each sale and purchase. Flat Rate Scheme is available to businesses with an annual VAT-inclusive turnover of £150,000 or less.

- VAT Cash Accounting Scheme: VAT is paid to HMRC when the customer settles their invoice rather than when it is issued under the Cash Accounting Scheme. Businesses also reclaim VAT when they pay their suppliers. The taxable turnover must be £1.35 million or less to join.

- VAT Annual Accounting Scheme: Businesses submit just one VAT return a year rather than four, making advance interim VAT payments throughout the year. Annual Accounting Scheme is available to businesses with a VAT-taxable turnover of £1.35 million or below.

- VAT Retail Schemes: VAT Retail Schemes simplify VAT calculations for retail businesses by allowing the use of average VAT rates for different products. This scheme means VAT does not need to be calculated for every individual sale. HMRC provides different retail scheme options based on business type.

- VAT Margin Scheme: The VAT Margin Scheme is designed for businesses dealing in second-hand goods, antiques, art, or collectables. VAT is charged on the difference between the buying and selling price rather than the full selling price.

What are the Pros and Cons of VAT?

The pros of VAT are discussed below.

- Reclaim VAT on purchases: Businesses can reclaim the VAT paid on business-related goods and services once registered. This reclaim results in major cost savings for businesses with significant expenditures.

- Improved credibility: VAT registration proves to customers and suppliers that a business is legitimate and established. This legitimacy is particularly beneficial when bidding for contracts or seeking new clients.

- Backdating registration: Newly registered businesses can backdate their registration by up to four years to reclaim VAT paid on business goods currently in use. Suitable evidence must be supplied for this process.

- Stable government revenue: VAT is considered a more stable source of income than tax on profits. Profits decline faster than turnover during economic slowdowns, which helps stabilise government finances.

- Better business opportunities: Some businesses only work with other VAT-registered businesses. Registering for VAT can open up opportunities and help a business expand.

The cons of VAT are listed below.

- Higher prices for customers: Charging VAT increases prices for customers who are not VAT-registered. These increased prices make products and services less competitive in the consumer market.

- Administrative burden: VAT-registered businesses must submit regular VAT returns, usually quarterly, requiring accurate and timely completion. Such a requirement adds administrative burden and demands careful financial planning.

- Risk of penalties: Late or missed VAT payments incur fines from HMRC. More late filings result in bigger fines, and bills increase quickly without careful management.

- Possible high VAT bill: A hefty VAT bill occurs if output VAT ends up considerably higher than input VAT. It is important to keep track of your accounts and save enough money.

- Complex rules: Maintaining detailed records for VAT purposes becomes time-consuming and costly. VAT also influences the pricing of goods and services in challenging ways.

What is the VAT in Tax Accounting?

VAT in tax accounting is the process of recording, reporting, and managing value-added tax across all business transactions. VAT-registered businesses deduct the VAT they have paid to other businesses from the VAT they have collected. Such a deduction confirms the tax remains neutral throughout the supply chain. Accurate value-added tax accounting is important for compliance, correct VAT returns, and accessing value-added tax services offered by HMRC.

Who Needs to Register for VAT?

Businesses exceeding the threshold of £90,000 in taxable turnover over the last 12 months must register for VAT. Registration is also necessary in case the turnover that is subject to tax is likely to amount to more than £90,000 in the coming 30 days. Businesses based outside the UK that supply any goods or services to the UK must also register, regardless of turnover.

The date from which VAT must be charged is not just the registration date, but the first day of the second month after exceeding the threshold. Voluntary registration is also available for businesses whose turnover falls below the threshold. This voluntary act allows them to reclaim VAT on business purchases and improve their credibility. Businesses whose taxable supplies are wholly or mainly zero-rated can apply for exemption from registration even if they exceed the threshold.

Who pays VAT?

VAT is paid by the end consumer when purchasing goods or services. Businesses collect VAT on behalf of the government at each stage of the supply chain, charging it to customers and remitting it to tax authorities. The financial burden usually falls on the final consumer, even though businesses handle VAT.

Is VAT considered an indirect tax?

Yes, VAT (Value Added Tax) is considered an indirect tax. It is applied to goods and services and collected by businesses on behalf of the government. The actual burden is passed on to consumers through prices. Indirect taxes like VAT are levied on consumption rather than income or profits.

What is a One-Stop Shop VAT?

OSS (One-Stop Shop) VAT is a system that allows businesses to register in one country. This system handles all their VAT reporting and payments for cross-border sales through a single online portal. The OSS system was introduced by the European Union to simplify compliance by avoiding multiple VAT registrations in different countries and centralising filing and payment.

Is it worth a small business being VAT registered?

It can be worth it for a small business, but it depends on circumstances. Benefits include reclaiming VAT on purchases and improving business credibility. It, however, also increases paperwork, costs, and sometimes raises prices for customers. Businesses should consider the pros and cons based on turnover, clients, and expenses before deciding.

✓ Free initial consultation