What Is a T-Account?

A T-account is an accounting tool used in double-entry bookkeeping to record financial transactions. It is a visual representation of a ledger account and looks like the letter T. The title of the account is above, the debit account is on the left of the T, and the credit account is on the right. This structure is more convenient for maintaining an account balance and keeping track of where the money is going.

Why Are T-Accounts Used in Accounting?

T-accounts are used in accounting to map, analyse, and confirm recording transactions through a clear division of transactions into debit (left) and credit (right) sides. This structure allows double-entry bookkeeping, in which all transactions impact at least two accounts. It ensures accuracy and makes it simple to establish the appropriate balance of accounts before making financial statements.

T-accounts are used in accounting with the following purposes and benefits that are explained below.

- Visualising Transactions: T-accounts give a clear format that assists the user in understanding the impact of each transaction on an account, both on the debit and credit sides.

- Debit Credits Balancing: They simplify the processes of making sure that total debits are equal to total credits, which is crucial in keeping proper records.

- Error Detection: T-accounts can be used to detect errors like missing entries or unequal totals by organising the entries.

- Tracking Account Changes: They help accountants track ups and downs in each account over time.

- Educational Aid: T-accounts are also used in learning, as they help beginners to understand the complex accounting concepts easily.

- Reconciling Records: They help make sure that financial data is accurate and consistent by comparing and checking accounts.

✓ Free initial consultation

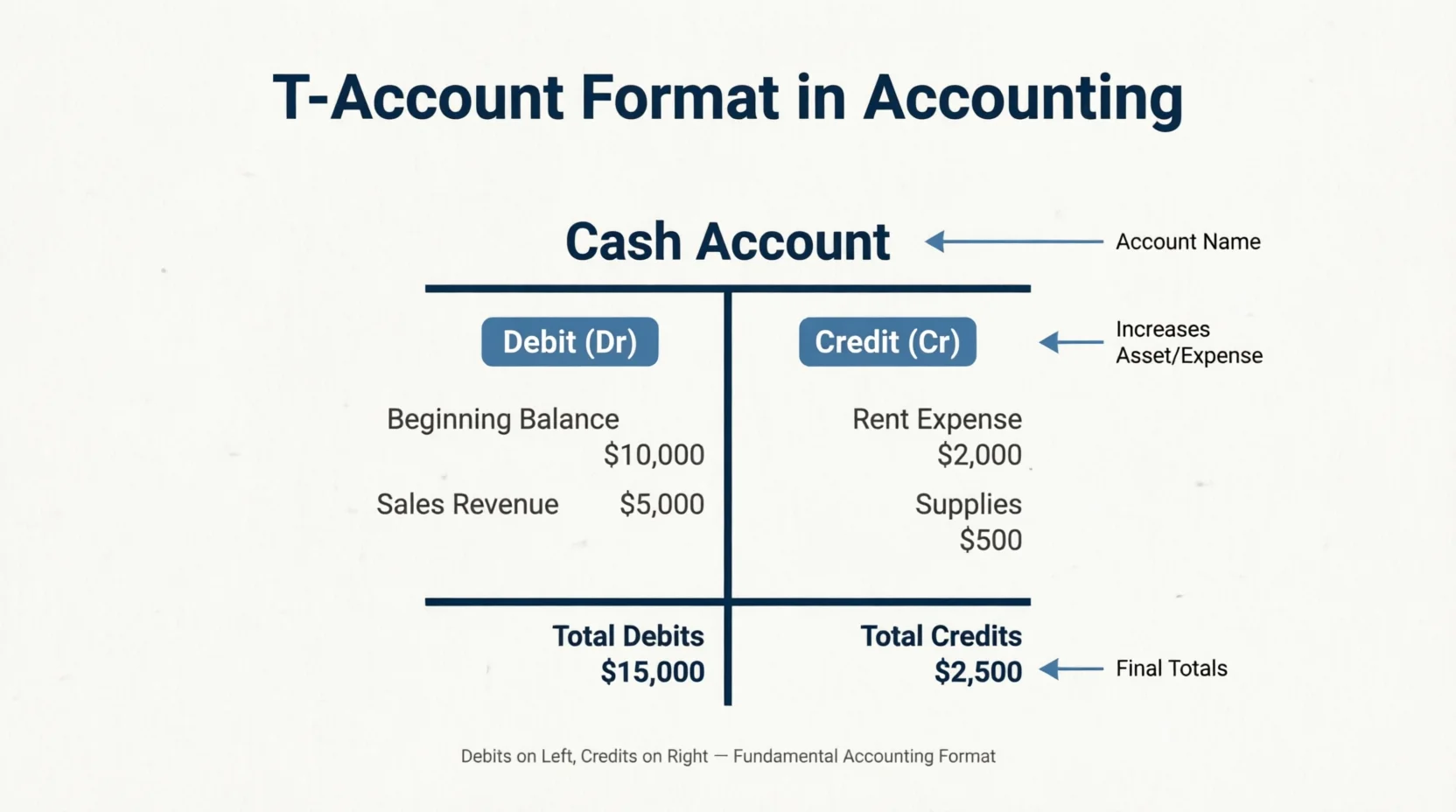

What Is the Format of a T-Account?

A T-account uses a simple T-shaped format to show how recording transactions affects an individual account. The account name is written at the top with the debit side on the left and the credit side on the right, forming a clear chart used in T-chart accounting to track increases and decreases.

All transactions affect at least two accounts in accounting. These transactions are subdivided into two sides by T-accounts to simplify their analysis. The debit side normally reflects the gains in assets and expenses, whereas the credit side reflects gains in liabilities, equity, and revenue. T-accounts facilitate the monitoring of account balance, the identification of errors, and the manner in which money circulates in a business.

The cash account is debited as money is received in the business in this chart, and this adds to assets. The service revenue account is credited because the business has earned income at the same time. This is a basic rule of double-entry bookkeeping, in which the sum of debits must equal the sum of credits to keep the accounts balanced. This format of T-chart accounting is widely presented in the educational materials since it is easy to visualise how transactions flow through accounts and helps prepare appropriate financial reporting.

What Are the Different Types of T-Accounts?

There are different types of T-accounts, and all of them are utilised to trace a particular financial activity. These types relate to the primary sets of accounts that are used when making transactions under the two-entry system in bookkeeping.

The different types of T-accounts and their uses include the following.

- Asset T-Accounts: These are the trackable resources of a business, like cash, equipment, and accounts receivable. The debit side is normally increased by assets, and the credit side is always decreased by assets.

- Liability T-Accounts: These show what a business owes to others, such as loans and accounts payable. Liabilities usually increase on the credit side and decrease on the debit side.

- Equity T-Accounts: These are the interests of the owner in the business, commonly known as the owner equity. They are used to follow investments, withdrawals and retained earnings, which are often on the credit side.

- Revenue T-Accounts: These record income that is received in the course of running a business, such as sales or service revenue. Revenue accounts are accrued and show revenues earned within a period on the credit side.

- Expense T-Accounts: These are records of expenses incurred to operate the business, like rent, salaries and utilities. The costs grow on the debit account and decrease the profitability.

How Do You Record Transactions in a T-Account?

Recording transactions in a T-account is not difficult once you understand the basic rules of debit and credit. All the financial transactions have impacts on two or more accounts in the double-entry system of bookkeeping, which keeps the accounting records balanced. T-accounts assist in recording transactions and make them easy to understand since they make it clear where each entry is.

Follow these steps to record transactions in a T-account.

Step 1: Identify the Accounts Affected.

Identify the accounts involved in the transaction. For example, a cash sale can have an impact on cash and revenue accounts.

Step 2: Use Debit and Credit Rules.

Decide which account should be debited and which should be credited. Debits tend to increase the assets and expenses, whereas credits tend to increase liabilities, equity and revenue.

Step 3: Fill in Amounts in the T-Accounts.

Enter the transaction amount to the correct side of each T-account. List the debits on the left-hand side and credits on the right-hand side.

Step 4: Compute the Balance.

Sum up both sides of the T-account and ascertain the balance. This helps make sure that the total debits equal the total credits and the accounts are correct.

What is an Example of a T Account?

An example of a T-account is that a small business receives the cash of 2,000 dollars as a payment for services provided on the same day. It impacts two accounts, such as cash increases (debit) and service revenue increases (credit).

Cash (Asset)

─────────────────────────────────────

Debit (+) | Credit ( −)

─────────────────────────────────────

Service Rev 2,000 |

─────────────────────────────────────

Balance: $2,000 Dr

Service Revenue (Revenue)

─────────────────────────────────────

Debit (−) | Credit (+)

─────────────────────────────────────

| Cash sale 2,000

─────────────────────────────────────

Balance: $2,000 Cr

Total Debits $2,000 = Total Credits $2,000

Assets and expenses increase on the debit (left) side. The credit (right) side shows an increase in revenue, liabilities and equity. Receipt of cash is a debit, since cash is an asset. The increase in revenue increases equity, and therefore, it is a credit to earn.

How Do T-Accounts Help in Preparing Financial Statements?

T-accounts help prepare financial statements by grouping financial activities into separate accounts. This grouping makes it easy for the organisation to extract the specific figures needed for the income statement, balance sheet, or closing balance of that particular period.

T-accounts assist in preparing the financial statements through the following methods.

- Organising transactions by account: Each transaction is documented in a T-account of its own, cash, rent expense, or accounts receivable. This separation gives the effect that when it comes to making a financial statement, all the accounts already have only what should be in them, with nothing combined. Consider each T-account as a labelled folder, and the filing cabinet is the general ledger. Accountants simply take out the folder they require to prepare a statement, without looking through a single stack of mixed transactions.

- Calculating account balances: The balance of all the T-accounts is determined by summing the debit side, summing the credit side, and subtracting the smaller of the two. As soon as all the transactions are recorded. This closing balance is the unique figure that goes directly into a line item of a financial statement. For example, when the Cash T-account has debits of 8,500 and credits of 3,200, the closing balance will be 5,300, and that is the same 5,300 that will be shown in the balance sheet as cash.

- Preparing the trial balance: A trial balance shows the ending balance of all T-accounts and a two-column list of all debit and credit balances. The books are in balance when the totals are the same, and the accountant can confidently start making the official financial statements. The trial balance is the entry point between T-accounts and financial statements. A total that is not equal is an indication of a recording error that needs correction before any report is issued. T-accounts allow one to trace and see where the difference in the accounts occurred.

- Supporting the income statement: The income statement is provided by all T-accounts of revenue and expenses. The balances in the revenue account are added together to generate total income. The balance of expense accounts is added to create total costs. The two are separated by the difference between the net profit or net loss of the period.

- Supporting the balance sheet: The balance sheet is supplied by asset, liability and equity T-accounts. The final balance of the Cash T-account is the Cash line. The T-account of Accounts Receivable is converted to the Accounts Receivable line. All the lines in a balance sheet are directly linked to one or more T-account closing balances. The equation Assets = Liabilities + Equity should always hold provided that all T-accounts have been balanced properly, since the use of the double-entry system implies that all the credit items have been debited elsewhere in the ledger.

✓ Free initial consultation

Can You Prepare Financial Statements Without Using T-Accounts?

Yes, you can prepare financial statements without using T-accounts. Financial transactions can be entered directly by accountants in a ledger, spreadsheets, or accounting software, which automatically calculates all account balances. T-accounts are a useful tool for preparing the balance sheet and other financial statements. They, however, are not a required step, as one can prepare these statements if accurate records of all transactions are maintained.

What Are the Rules for Debit and Credit in a T-Account?

The rules for debit and credit in a T-account depend on the type of account. Debits always represent the left side, and credits represent the right side in a T-account. Debits increase assets and expenses but decrease liabilities, equity, and revenue. Credits increase liabilities, equity, and revenue but decrease assets and expenses. Debits must always equal credits to maintain the accounting equation.

How Do You Balance a T-Account?

To balance a T-account, add up the amounts on both the debit (left) and credit (right) sides. Then, find the difference and enter that amount as a “balance carried down” on the smaller side so that both sides add up to the same amount. Finally, move this balance to the other side of the total line, below it, to start the next period.

Can a T-Account Have a Negative Balance?

A T-account does not show a negative number, but it can carry a balance on the opposite side of its normal balance, which some people refer to as a negative balance. An asset account or expense account normally holds a debit balance, so a credit balance on either would be considered unusual, signalling an error or an abnormal transaction.

What Is the Difference Between a T-Account and a General Ledger?

The difference between a T-account and a general ledger is that a T-account is a simple visual representation of a single account using a T-shaped format, showing the debit side and credit side of individual transactions. A general ledger is the complete official record containing every account in the business.

The differences between a T-account and a general ledger are listed below.

- Purpose: A T-account visually shows how transactions impact a single account, while the general ledger is the official record of all accounts and transactions for audits and reports.

- Structure: T-accounts are T-shaped, with debits on the left and credits on the right. Each account has its own T. A general ledger includes columns for date, description, reference number, debit, credit, and running balance.

- Usage: A t-account is used informally to plan entries before posting, explain double-entry concepts, or troubleshoot a recording error. A general ledger is used formally in daily bookkeeping, period-end closing, and as the primary source when preparing financial statements.

- Scope: T-accounts focus on individual accounts. A general ledger consolidates all accounts, including assets, liabilities, equity, revenue, and expenses.

- Level of detail: A T-account shows only the amount and a brief label, and lacks dates and running balances. A general ledger provides comprehensive details, including dates, descriptions, and a running balance.

- Role in the accounting process: T-accounts help understand the accounting cycle, while the general ledger is crucial for formal accounting. Journal entries in the general ledger lead to the trial balance and financial statements.

- Practical use: A T-account can be quickly drawn to show transactions or troubleshoot accounts. A general ledger is managed in accounting software, automatically updating with each journal entry.

What Is the Difference Between a T-Account and a Journal Entry?

The difference between a T-account and a journal entry is that a T-account is a visual tool that shows how a single transaction affects an individual account’s balance. A journal entry is the first official record of a transaction entered into the accounting records in chronological order.

The differences between a T-account and a journal entry are discussed below.

- Purpose: A T-account is a visual representation used to show how debit and credit entries affect the balance of one individual account. A journal entry is the first official record of a financial transaction, capturing what happened, which accounts were affected, and by how much.

- Position in the Accounting Process: A journal entry is recorded first when a financial transaction occurs, followed by a T-account, which visualises the effects of those entries.

- Format: T-accounts are drawn as a T-shape with the account name at the top, debit entries on the left, and credit entries on the right. No dates or references required. A journal entry is written in a structured format showing the date, the accounts debited and credited, the amounts, and a brief narration explaining the transaction.

- Level of Detail: A T-account shows only the amount and a short label per entry. There is no date, no narration, and no journal reference number. A journal entry includes full details, such as the transaction date, account names, debit and credit amounts, and a narration describing the nature of the transaction.

- Number of accounts: Each T-account covers only one account. Draw a separate T for every account involved to see the full effect of a transaction. A single journal entry captures all accounts affected by one transaction together in one place, both the debit and credit sides in one entry.

- Use in accounting system: A T-account is an informal tool for analysis, not part of official records. A journal entry is essential, recording every financial transaction before posting to the ledger.

- Practical usage: T-accounts help students and accountants visualise transactions. Journal entries record every financial transaction, such as sales and payroll.

What Is the Difference Between a T-Account and a Balance Sheet?

The difference between a T-account and a balance sheet is that a T-account is a tool used to record and analyse individual account transactions. A balance sheet is a financial statement that summarises all account balances to show a company’s financial position.

The differences between a T-account and a balance sheet are mentioned below.

- Purpose: A T-account is used to track debits and credits of a single account, and a balance sheet is used to present the overall financial position at a specific time.

- Type of Record: A T-account is an internal accounting record, while a balance sheet is an external financial statement prepared for reporting.

- Scope: A T-account focuses on one account, whereas a balance sheet combines all account balances into assets, liabilities, and equity.

- Structure: A T-account is shaped like a “T” with two sides, and a balance sheet is organised into categorised financial sections.

- Stage in Accounting Process: A T-account is used during transaction recording, while a balance sheet is prepared after completing the accounting cycle.

- Level of Detail: A T-account shows detailed entries, but a balance sheet presents summarised financial data.

- Usage: T-accounts are used by accountants for analysis and adjustments, while a balance sheet is used by investors, creditors, and management for decision-making.

What Are the Advantages of Using T-Accounts?

The advantages of using T-accounts are easy to understand, provide a clear view of transactions, help track account changes, and are useful for learning accounting. Other benefits are simplified error detection and improved transaction analysis.

The advantages of using T-accounts are given below.

- Easy to understand: T-accounts are simple, clearly showing debit and credit entries for beginners.

- Clear view of transactions: They provide a structured layout, which improves transaction tracking and visibility.

- Helps track account changes: T-accounts show how balances change after each transaction.

- Useful for learning accounting: They build strong foundations in account analysis and double-entry concepts.

- Simplifies Error Detection: Imbalances in debit and credit entries help quickly identify mistakes.

- Improves transaction analysis: T-accounts allow a detailed review of each entry for better account analysis.

What Are the Disadvantages of Using T-Accounts?

The disadvantages of using T-accounts are limited detail, impracticality for large businesses, no automatic balancing, difficulty tracking many accounts, and a manual process.

What Are Common Mistakes When Using T-Accounts?

Common mistakes when using T-accounts include reversing debits and credits, and misunderstanding normal balances. Forgetting double-entry, misclassifying accounts, ignoring adjusting entries, and errors in calculation.

What Can Professional Accountants Do for Your T-Accounts?

Professional accountants help manage T-accounts by accurately recording financial transactions while confirming correct posting entries on the debit and credit sides. They maintain correct account balances for each ledger account. Managing T-accounts can be confusing and time-consuming for small business owners. Professional accounting services make sure all entries are properly recorded and balanced, and keep financial records up to date.

How Can Online Bookkeeping Help You With T-Accounts?

Online bookkeeping services have made it much easier for businesses to manage their T-accounts. These platforms make sure each ledger account is updated accurately by automating the recording of financial transactions. Such services reduce manual errors and provide a clear, real-time view of account balances for better financial management.

✓ Free initial consultation