What is a Journal Entry?

A journal entry is the chronological record of a financial transaction in a company’s general journal, serving as the first step in the accounting cycle. Every journal entry uses the double-entry system to record equal amounts of debit and credit, ensuring the accounting equation remains balanced at all times.

Accounting journal entries capture every financial event, from sales revenue to expense payments, in a structured format. Each journal entry includes the description of the journal transaction, the date of the transaction, the accounts affected, the debit and credit amounts, and a brief narration describing the journal transaction. The double-entry system requires that every journal entry affect a minimum of 2 accounts. One account receives a debit, and and Second account receives a credit.

The relationship between a journal entry and the accounting equation is direct. Every debit and credit recorded in a journal entry maintains the balance of the accounting equation. Revenue recognition, the expense matching principle, and accrual accounting standards govern when and how accounting journal entries are recorded in the general journal.

What Are the Types of Journal Entries?

Journal entries are classified into 8 primary types based on their purpose, frequency, and method of recording within the accounting cycle.

The main types of journal entries are listed below:

- Standard journal entry: records routine business transactions such as sales, purchases, and payments following the standard debit and credit rules of the double-entry system.

- Recurring journal entry: records transactions that repeat at fixed intervals, such as monthly rent, insurance premiums, and subscription fees, reducing manual effort in the accounting cycle.

- Manual journal entry: records transactions entered by an accountant without automation, typically used for non-routine adjustments and period-end closing entries.

- Automated journal entry: records transactions generated by accounting software based on pre-configured rules, improving accuracy and reducing human error in transaction recording.

- Correction entry: reverses or adjusts errors found in previously recorded journal entries, ensuring the trial balance and financial statements remain accurate.

- Allocation entry: distributes costs across multiple departments, projects, or cost centers, commonly used in cost accounting for overhead distribution.

- Payroll entry: records employee wages, salaries, tax withholdings, and benefits as part of payroll processing.

- Depreciation entry: records the systematic reduction of a fixed asset’s value over its useful life, calculated using methods such as straight-line or declining balance.

Journal entries include the amortization entry (used for intangible assets), simple journal entry (involving only 2 accounts), and compound journal entry (involving 3 or more accounts). Each type of journal entry follows the same debit and credit structure of the double-entry system while serving a distinct purpose in the accounting cycle.

What is the Format of a Journal Entry?

The journal entry format consists of 5 essential columns, date, account titles column, narration, debit amount, and credit amount.

The standard journal entry format is structured as follows:

| Column | Column 2 |

|---|---|

| Date | Records the exact date of the transaction. |

| Account Titles | Lists the accounts affected (debit first, credit indented below). |

| Narration | Provides a brief explanation of the transaction. |

| Debit (£) | Shows the amount debited to the relevant account. |

| Credit (£) | Shows the amount credited to the relevant account. |

How Does a Journal Entry Work?

A journal entry converts a financial transaction from source documents into a structured debit and credit record in the general journal, following the rules of the double-entry system.

The journal entry process consists of 6 sequential steps:

- Identifying the source documents: Collecting invoices, receipts, bank statements, or contracts that provide evidence of the financial transaction.

- Analyzing the transaction: Determining which accounts are affected and classifying each account as an asset, liability, equity, revenue, or expense under the accounting equation.

- Applying the debit and credit rules: Deciding which account receives a debit and which account receives a credit based on the double-entry system.

- Recording the journal entry: Entering the date, account titles, amounts, and narration in the general journal using the standard journal entry format.

- Completing ledger posting: Transferring the journal entry data from the general journal to the individual accounts in the ledger.

- Verifying through trial balance: Ensuring all debit and credit totals match in the trial balance to confirm the accuracy of the journal entry.

The journal entry process operates within the broader accounting cycle. After transaction recording, the journal entry flows through ledger posting, trial balance preparation, adjusting entries, and period-end closing. Revenue recognition and the expense matching principle determine the timing of journal entries under accrual accounting. Cash accounting records journal entries only when cash changes hands.

Internal controls govern the journal entry process by requiring authorization, documentation, and review before a journal entry is posted to the ledger. These internal controls prevent errors and fraud in the transaction recording process.

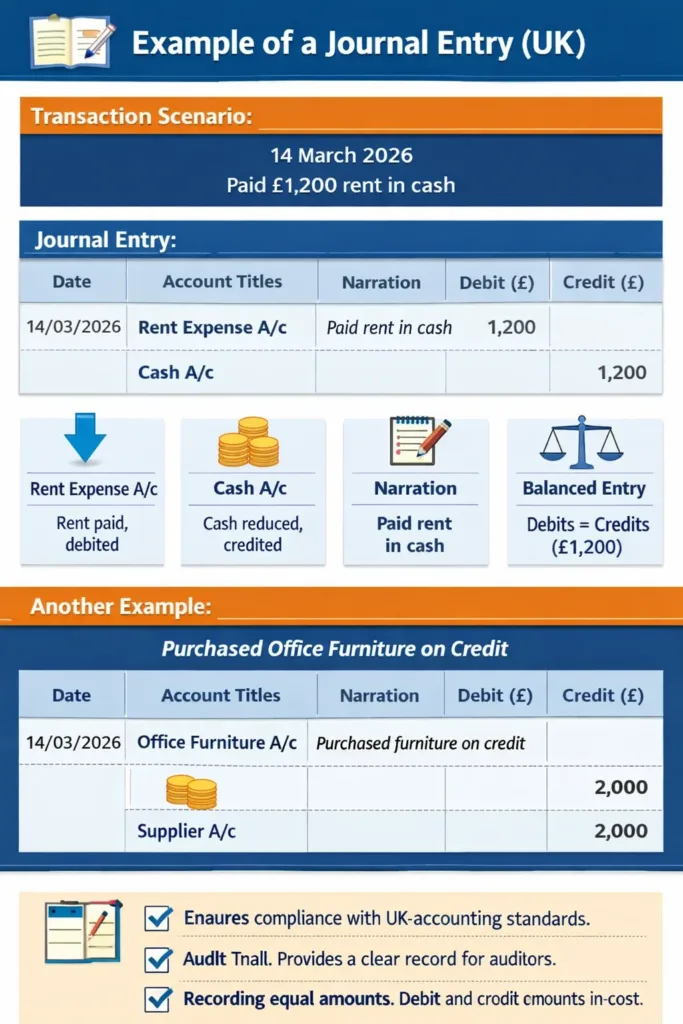

What is an Example of a Journal Entry?

Scenario: On 14 March 2026, a business pays £1,200 in cash as rent.

| Date | Account Titles | Narration | Debit (£) | Credit (£) |

|---|---|---|---|---|

| 14/03/2026 | Office Furniture A/c | Purchased furniture on credit | 2,000 | |

| Supplier A/c | 2000 |

Why Are Journal Entries Important in Accounting?

Journal entries are the foundation of the entire accounting cycle, providing the primary record from which all financial statements, trial balance reports, and regulatory filings originate.

The importance of journal entries in accounting spans 7 critical areas:

- Maintaining the accounting equation, every journal entry ensures Assets = Liabilities + Equity remains balanced through equal debit and credit amounts.

- Enabling accurate ledger posting, journal entries provide the source data transferred to individual ledger accounts during ledger posting.

- Supporting trial balance preparation, the trial balance summarizes all debit and credit balances from ledger posting, and accurate journal entries ensure the trial balance balances correctly.

- Facilitating financial consolidation, multi-entity organizations rely on standardized journal entries for accurate financial consolidation across subsidiaries and divisions.

- Ensuring period-end closing accuracy, period-end closing entries (revenue closing, expense closing, and dividend closing) depend on accurate journal entries recorded throughout the accounting period.

- Enforcing internal controls, journal entries create an audit trail that supports internal controls, fraud prevention, and regulatory compliance.

- Applying accounting principles, journal entries enforce revenue recognition, the expense matching principle, and accrual accounting standards in every transaction recording.

Journal entries transform raw financial data from source documents into structured records that flow through the entire accounting cycle. Without accurate journal entries, the trial balance, financial statements, and financial consolidation processes produce unreliable results. Cost accounting, payroll processing, and depreciation tracking all depend on precise journal entry recording.

How Journal Entries Are Used in Bookkeeping Systems?

Journal entries are the foundation of bookkeeping systems because they provide a chronological record of all financial transactions. Each entry captures the date, accounts involved, and the corresponding debits and credits, ensuring the double-entry principle is maintained. By recording transactions in this structured way, journal entries make it possible to transfer information into ledgers, prepare trial balances, and ultimately generate accurate financial statements. In short, they serve as the bridge between daily business activities and organized financial reporting, keeping the accounting equation balanced and the books reliable.

What is Debit and Credit in a Journal Entry?

Debit and credit are the 2 fundamental components of every journal entry in the double-entry system, representing increases or decreases in account balances based on the account type. The debit and credit rules in a journal entry follow the double-entry system principles listed below:

- Assets: a journal entry debit increases the asset balance; a journal entry credit decreases the asset balance.

- Liabilities: a journal entry debit decreases the liability balance; a journal entry credit increases the liability balance.

- Equity: a journal entry debit decreases equity; a journal entry credit increases equity.

- Revenue: a journal entry debit decreases revenue; a journal entry credit increases revenue.

- Expenses: a journal entry debit increases the expense balance; a journal entry credit decreases the expense balance.

The debit and credit amounts in every journal entry must be equal. This equality is the core mechanism of the double-entry system that maintains the accounting equation. The trial balance verifies this equality by comparing total debit and credit balances across all accounts after ledger posting.

Every journal entry records debit and credit on opposite sides. The debit side appears first (left column), and the credit side appears second (right column, indented). This debit and credit structure applies to all types of journal entries, standard journal entries, correction entries, payroll entries, depreciation entries, and amortization entries.

What Are the Components of a Journal Entry?

A journal entry is made up of several key components that ensure transactions are recorded clearly and accurately in bookkeeping systems. These include date, account titles, debit amount, credit amount, and narration.

More components found in modern accounting systems include the journal entry reference number, posting reference (linking to ledger posting), and approval status (supporting internal controls). These components ensure traceability throughout the accounting cycle.

What is the Difference Between Single and Double-entry Bookkeeping?

Single-entry bookkeeping records each transaction in 1 account, while double-entry bookkeeping records every transaction in 2 or more accounts using the debit and credit system.

The 5 key differences between single-entry and double-entry bookkeeping are listed below:

| Feature | Single-Entry Bookkeeping | Double-Entry Bookkeeping |

|---|---|---|

| Accounts affected | 1 account per transaction | Minimum 2 accounts per journal entry |

| Debit and credit | Not used | Required for every journal entry |

| Accounting equation | Not maintained | Always balanced |

| Trial balance | Cannot be prepared | Prepared from ledger posting data |

| Error detection | Limited | Strong, the trial balance reveals imbalances |

Double-entry bookkeeping is the standard method used in professional accounting. Every journal entry in the double-entry system affects a minimum of 2 accounts, ensuring the accounting equation remains balanced. Single-entry bookkeeping is suitable only for very small businesses with minimal transactions.

The double-entry system supports the complete accounting cycle, from transaction recording and ledger posting to trial balance preparation, financial consolidation, and period-end closing. Single-entry bookkeeping lacks the structure required for these processes.

What is the difference between a journal entry and a Ledger?

A journal entry is the first chronological record of a transaction, while a ledger is the organized collection of individual accounts where journal entry data is posted.

The 4 key differences between a journal entry and a ledger are listed below:

| Feature | Journal Entry | Ledger |

|---|---|---|

| Order | Chronological (by date) | Organized by account |

| Purpose | Records transactions as they occur | Summarizes all transactions per account |

| Stage in the accounting cycle | First step, transaction recording | Second step, ledger posting |

| Format | Date, account titles, debit, credit, narration | Account name, debit column, credit column, balance |

The journal entry captures the initial transaction recording using source documents. Ledger posting transfers each debit and credit from the journal entry to the corresponding account in the ledger. The trial balance then summarizes all ledger account balances to verify accuracy.

Journal entries and ledger accounts are interdependent stages of the accounting cycle. Accurate journal entries produce accurate ledger postings, which produce an accurate trial balance. Errors in journal entries cascade through the entire accounting cycle.

What is the difference between a journal entry and a Transaction?

The difference between a transaction and a journal entry lies in their role within the accounting process. A transaction is the actual business event that affects a company’s finances, for example, selling goods, paying rent, or receiving cash. It represents the real-world exchange of value. A journal entry, on the other hand, is the formal record of that transaction in the accounting system. It translates the event into accounting terms by specifying which accounts are debited and credited, along with the amounts and a description. In short, the transaction is the event itself, while the journal entry is the structured documentation of that event in the books.

How to Record Journal Entries?

To record journal entries, follow a clear step-by-step process:

- Identify the transaction: Collect source documents such as invoices, receipts, or payroll records.

- Determine accounts affected: Decide which accounts increase or decrease, and classify them as assets, liabilities, equity, revenue, or expenses.

- Apply the debit and credit rule: Record debits and credits according to the double-entry principle, ensuring they balance.

- Write the entry in the general journal: Include the date, account titles, debit and credit amounts, and a short description of the transaction.

- Post to the general ledger: Transfer the journal entry into the ledger, where transactions are grouped by account.

- Review for accuracy: Check that debits equal credits and that accounts are properly classified before preparing trial balances and financial statements.

This structured approach ensures every financial event is documented correctly and provides a reliable foundation for bookkeeping.

What Are Common Journal Entry Mistakes?

Common journal entry mistakes often occur when transactions are recorded inaccurately or incompletely. Some frequent errors include misclassifying accounts, forgetting to balance debits and credits, which disrupts the accounting equation. Another mistake is using vague or missing descriptions, making it hard to trace the purpose of an entry later.

How Can Xact+ Accountant Help With Journal Entries?

Xact+ Accountant helps with journal entries by automating the recording process, reducing human error, and ensuring compliance with the double-entry bookkeeping system. It streamlines tasks like posting invoices, payments, and adjustments directly into the general journal, saving accountants time and improving accuracy.

- Automation of Entries: Converts transactions such as invoices, bills, payroll, and reconciliations into journal entries automatically.

- Double-Entry Compliance: Ensures every debit has a corresponding credit, keeping the accounting equation balanced.

- Custom Journal Entries: Allows accountants to create adjusting, correcting, or special entries when needed.

- Integration with Modules: Links journal entries with sales, purchases, inventory, and payroll, preventing duplication.

- Audit Trail: Provides detailed descriptions and references for each entry, making them easy to trace during audits.

- Error Reduction: Minimizes manual mistakes by standardizing entry formats and calculations.

- Efficiency: Saves time by streamlining repetitive bookkeeping tasks.

- Reporting Accuracy: Supplies clean, reliable data for preparing trial balances and financial statements.

How Do Payroll Services Affect Journal Entries?

Payroll services affect journal entries by creating structured records of employee compensation, deductions, and employer contributions. They generate entries that debit expense accounts such as salaries, wages, or payroll taxes, and credit liability accounts.