The history of accounting spans over 7,000 years, with the origin of accounting rooted in the ancient civilisations of Mesopotamia, Egypt, and Rome. The evolution of accounting moved from simple clay tablet records to the double-entry bookkeeping system formalised by Luca Pacioli in 1494, laying the foundation for modern accounting as practised by every UK company, accountant, and financial professional today.

Accounting is the systematic process of recording, classifying, and reporting financial transactions — and understanding its origins reveals why accounting remains the backbone of every business, from sole traders managing a calendar month of receipts to large corporations preparing statements aligned with the financial year end. The development of accounting through ancient, medieval, and industrial eras shaped the 5 main branches of accounting used today: financial accounting, management accounting, cost accounting, tax accounting, and auditing.

The double-entry bookkeeping system, first documented in the 15th century, revolutionised how UK companies record assets, liabilities, and equity for accounting purposes. Modern accounting integrates International Financial Reporting Standards (IFRS), technology platforms, and structured compliance frameworks, including the financial year UK rules governing when a business year end falls and how financial statements must be filed.

Bookkeeping, though often conflated with accounting, serves a distinct role in recording day-to-day transactions, while accounting provides the analytical layer that turns those records into strategic financial intelligence.

What is the History of Accounting?

The history of accounting is the 7,000-year record of how human civilisations developed systems to track, report, and analyse financial transactions.

The origin of accounting predates currency itself. Ancient peoples recorded grain stores, livestock counts, and labour exchanges on clay tablets long before coins existed. The founder of accounting as a formal discipline is widely recognised as Luca Pacioli, an Italian mathematician who published the first comprehensive description of the double-entry bookkeeping system in 1494, a method still central to modern accounting and used by every UK company preparing records for the financial year end.

The evolution of accounting accelerated through 4 major historical periods: ancient record-keeping (5000 BCE onward), medieval Italian commerce (1200s–1500s), the Industrial Revolution (1760–1840), and the digital era (1980s to present). Each period introduced new demands for accuracy, transparency, and standardisation.

Modern accounting operates within a structured regulatory environment. In the United Kingdom, the financial year framework requires UK companies to file accounts within 9 months of their business year end, using standards set by the Financial Reporting Council (FRC) and aligned with IFRS. These standards are the direct descendants of principles formalised across the long history of accounting.

What is the Origin of Accounting?

The origin of accounting traces to Mesopotamia around 3000 BCE, where Sumerian scribes recorded grain and cattle transactions on clay tablets using a system of tokens and pictographs.

These early records were not created for accounting purposes in the modern sense. They were administrative tools used by temple priests and palace officials to manage resource distribution. The origin of accounting is therefore inseparable from the origin of governance and trade.

Ancient Egypt refined accounting between 3000 and 2000 BCE, with royal scribes maintaining detailed records of state revenues. Construction costs and agricultural outputs across each calendar month of the harvest cycle. The Egyptian model introduced a proto-audit system where independent scribes cross-checked records. A principle still embedded in modern financial year-end audit procedures used by every UK company today.

The Romans formalised accounting further between 500 BCE and 400 CE. Roman households maintained an “adversaria” (daily transaction log) and a “codex” (monthly summary), creating the first structured distinction between day-to-day bookkeeping and periodic financial reporting. A distinction that now separates bookkeeping from accounting in the UK financial year regulatory framework.

The formal founder of accounting as a documented discipline is Luca Pacioli (1447–1517), whose 1494 work “Summa de Arithmetica”. It includes the first printed description of the double-entry bookkeeping system. Pacioli did not invent the method but codified the practices used by Venetian merchants, making the origin of accounting as a teachable, transferable discipline a 15th-century achievement.

How Did Accounting Start in Ancient Civilisations?

Accounting in ancient civilisations started as a tool for resource management. The development of accounting was driven by the need to track surpluses, debts, and obligations across growing populations.

Accounting in Mesopotamia is the earliest documented example of systematic financial record-keeping. Sumerian temple administrators used clay tablets inscribed with cuneiform script to log trade records covering grain loans, silver payments, and labour allocations. Over 500,000 of these tablets have survived, forming the oldest accounting archive in human history.

The development of accounting in Mesopotamia introduced 3 foundational concepts still present in modern accounting:

the recording of dates (equivalent to today’s calendar month entries), the identification of parties to each transaction, and the documentation of quantities or values exchanged. These three elements form the core of every journal entry made by a UK company for accounting purposes today.

Ancient Chinese accounting records from the Zhou Dynasty (1046–256 BCE) show parallel development, with government officials maintaining separate accounts for revenues and expenditures. Mirroring the debit-credit structure later formalised in the double-entry bookkeeping system.

The ancient trade records of the Indus Valley Civilisation (2600–1900 BCE) demonstrate standardised weights and measures used in commerce. An early form of accounting standardisation that preceded the uniform reporting frameworks of the modern financial year-end by nearly 4,000 years.

The development of accounting in medieval Europe accelerated between 1200 and 1494 CE, driven by the expansion of Italian merchant banking. Florentine and Venetian traders needed reliable trade records to manage credit and partnerships. And overseas commerce across multiple calendar months and trading seasons. This commercial pressure produced the double-entry bookkeeping system, which Luca Pacioli documented and published for the first time in 1494.

What is the Evolution of Accounting?

The evolution of accounting follows 5 distinct phases:

ancient record-keeping, medieval double-entry development, Industrial Revolution standardisation, 20th-century professionalisation, and digital-era automation.

Phase 1: Ancient Record-Keeping (5000–500 BCE): Accounting in Mesopotamia, Egypt, and China produced the first trade records. These were single-entry systems focused on resource tracking without formal balance concepts.

Phase 2: Medieval Double-Entry System (1200–1600 CE): The development of accounting in Italian city-states produced the double-entry bookkeeping system. Luca Pacioli formalised the system in 1494, introducing the concepts of debits, credits, ledgers, and trial balances — concepts unchanged in modern accounting.

Phase 3: Industrial Revolution Standardisation (1760–1900): Rapid industrialisation created demand for consistent financial reporting across large enterprises. The first professional accounting bodies formed during this period were the Institute of Chartered Accountants in Scotland (ICAS) in 1854 and the Institute of Chartered Accountants in England and Wales (ICAEW) in 1880. The financial year, the UK concept of a fixed business year end for corporate reporting, became standard practice during this era.

Phase 4: 20th-Century Professionalisation (1900–1980): International standards emerged. The International Accounting Standards Committee (IASC), founded in 1973, began harmonising global accounting practices. Every UK company became subject to statutory requirements linking accounting to the financial year-end, tax planning, and auditing.

Phase 5: Digital Automation (1980–Present): Software platforms replaced manual ledgers. Modern accounting now integrates real-time data, cloud-based reporting, and artificial intelligence. The financial year-end for a UK company can now be closed and filed digitally within days rather than the calendar months it once required.

Why Is Accounting Important?

Accounting is important because it provides the financial intelligence that enables businesses to make decisions and meet legal obligations. Accounting plan taxes, and demonstrate financial health to investors, lenders, and regulators.

Every UK company depends on accounting for 4 core purposes: compliance with the financial year-end filing requirements of Companies House. HMRC, accurate tax planning to minimise liabilities legally, performance measurement across each calendar month of trading, and strategic planning based on historical and projected financial data.

Accounting generates the financial statements that external stakeholders, banks, investors, HMRC, and directors use to evaluate a business. Without reliable accounting, a UK company cannot secure financing, pass an audit, or demonstrate solvency at the financial year-end.

The financial year rules require UK companies to produce a balance sheet, profit and loss account, and notes to the accounts for each business year end. These documents are the direct output of the accounting system and the primary evidence used in tax planning and investor relations.

What Are the Different Main Types of Accounting?

Different main types of accounting include financial accounting, management accounting, cost accounting, tax accounting, and auditing, each serving a distinct purpose in how a business records and reports financial activity. The main types of accounting are listed below:

- Financial accounting: producing financial statements (balance sheet, income statement, cash flow statement) for external stakeholders at the financial year end

- Management accounting: generating internal reports to support decision-making across each calendar month of trading

- Cost accounting: analysing production and operational costs to improve profitability for a UK company

- Tax accounting: preparing accurate tax returns and executing tax planning strategies aligned with the financial year UK framework.

- Auditing: independently verifying the accuracy of financial statements produced for accounting purposes

Each type of accounting requires distinct skills, qualifications, and tools. Financial accounting and tax accounting are the most directly regulated types for any UK company, as both feed directly into business year-end filings with Companies House and HMRC.

What is the Double-Entry Bookkeeping System?

The double-entry bookkeeping system is the accounting method in which every financial transaction is recorded in 2 separate accounts. A debit in one account and an equal credit in another, ensuring the accounting equation (Assets = Liabilities + Equity) always balances.

Luca Pacioli documented the double-entry bookkeeping system in 1494, and it has remained the global standard for accounting ever since. Every UK company, regardless of size or sector, uses the double-entry bookkeeping system to prepare the financial statements required at the business year-end.

The double-entry bookkeeping system enables effective tax planning because the structured ledger produces an accurate picture of taxable income, deductible expenses, and asset values, all of which are required for the UK tax return process.

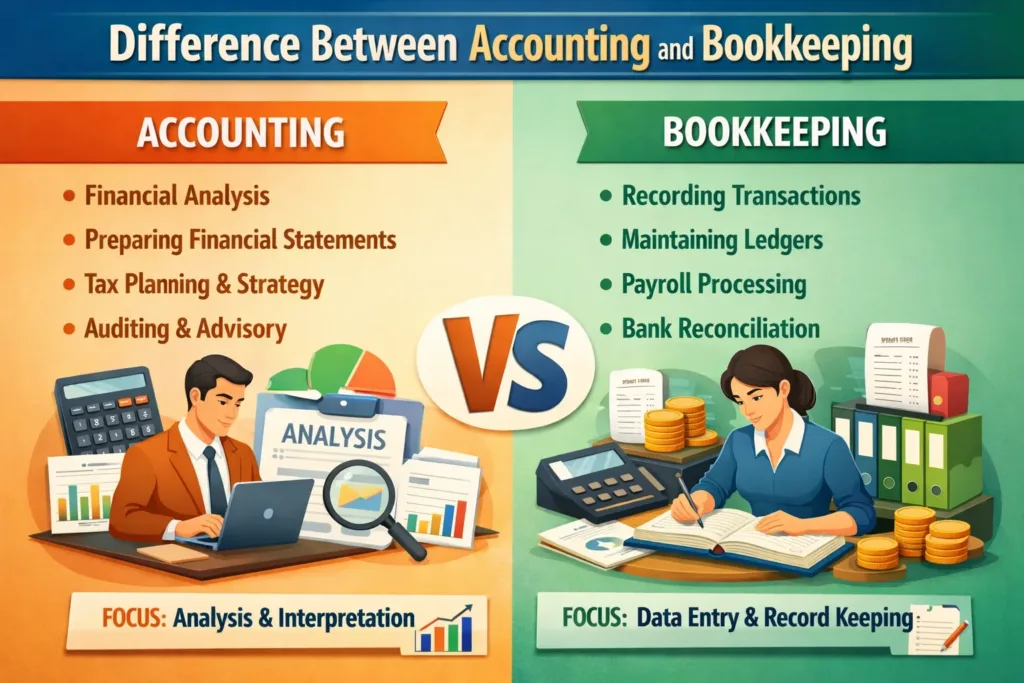

What is the Difference Between Accounting and Bookkeeping?

Accounting is the broader discipline of classifying, analysing, interpreting, and reporting those transactions for decision-making and compliance. Accounting transforms that data into financial statements, tax returns, and strategic insights used by every UK company at the financial year-end.

Bookkeeping is the process of recording daily financial transactions. Bookkeeping produces the raw data, invoices, receipts, payroll records, and bank entries recorded calendar month by calendar month.

What is the Difference Between Traditional Accounting and Modern Accounting?

Traditional accounting relies on manual ledgers, paper-based records, and periodic reporting. Modern accounting uses software platforms, real-time data, and automated compliance tools to produce financial statements continuously.

Traditional accounting required accountants to manually post every transaction, reconcile ledgers at the end of each calendar month, and compile financial statements by hand at the business year-end. The process was time-intensive, error-prone, and limited the frequency of financial insights available to business owners.

Modern accounting automates the double-entry bookkeeping system through platforms such as Xero, Sage, and QuickBooks. A UK company using modern accounting tools can generate management accounts at any point in the financial year, prepare for the financial year end in real time, and submit digital tax returns directly to HMRC through Making Tax Digital (MTD) compliant software.

What is the Difference Between Financial Accounting and Management Accounting?

Financial accounting produces standardised financial statements for external stakeholders at the financial year end, while management accounting produces internal reports used by business leaders to guide operational decisions throughout the trading year.

Financial accounting is backwards-looking, reporting what happened during a defined period ending at the business year-end. Financial accounting follows strict standards (UK GAAP or IFRS), and every UK company must produce financial statements for accounting purposes and file these with Companies House within the statutory deadline.

Management accounting is forward-looking, producing budgets, forecasts, variance analyses, and performance dashboards for internal use. Management accounting reports are not regulated by the financial year UK framework and can be produced for any period, weekly, calendar month, or quarterly, based on the business’s needs.

How Does Accounting Help Businesses?

Accounting helps businesses by providing the financial data needed to make informed decisions, manage cash flow, comply with tax obligations, and demonstrate financial viability to lenders and investors.

Accounting increases business profitability by identifying cost inefficiencies, tracking revenue trends across each calendar month, and providing the tax planning insights that reduce a UK company’s overall tax burden legally and accurately.

The 6 core ways accounting helps businesses are listed below:

- Cash flow management: tracking inflows and outflows across each calendar month to prevent insolvency.

- Tax planning: structuring income, expenses, and timing to minimise tax liability at the financial year end.

- Regulatory compliance: meeting the financial year UK requirements for Companies House and HMRC filings.

- Investment readiness: producing the audited financial statements required by banks and investors.

- Performance measurement: comparing actual results against budgets using management accounting reports.

- Strategic planning: using historical financial data to forecast future revenue, costs, and capital needs

Why Does a Business Need a Bookkeeper?

A business needs a bookkeeper to ensure every financial transaction is recorded accurately across each calendar month. Bookkeeper creating a clean and complete data set that accountants require to produce financial statements and tax returns at the business year-end.

Without accurate bookkeeping, the accounting process breaks down. A UK company that fails to maintain proper records across the financial year period faces penalties for inaccurate financial statements and failed audits. The bookkeeper is the foundation upon which all accounting, tax planning, and financial year-end reporting is built.

The 5 primary responsibilities of a bookkeeper are listed below:

- Recording all sales invoices, purchase invoices, and receipts into the accounting system daily or weekly

- Reconciling bank statements against the ledger at the end of each calendar month

- Processing payroll and ensuring PAYE submissions are accurate and timely

- Maintaining VAT records and preparing VAT returns aligned with the UK financial year reporting calendar

- Providing trial balances and supporting documentation to the accountant before the business year-end

The distinction between bookkeeping and accounting for a UK company is a division of labour. Bookkeepers maintain the day-to-day records, and accountants apply expertise to those records for accounting purposes and financial year-end compliance. Both roles are essential to the financial health of any business.