The general ledger is a master accounting record that organizes all financial transactions by individual ledger accounts, and the general journal is the initial book of entry where every financial transaction is recorded in chronological order using debit and credit format. The general ledger and the general journal serve 2 distinct but interconnected roles within a double-entry accounting system. The general journal captures raw financial transactions as journal entries, and the general ledger classifies those journal entries into specific account categories such as assets, liabilities, equity, revenue, and expenses. Understanding the difference between a ledger vs journal is essential for accurate bookkeeping, reliable financial reporting, and maintaining organized accounting records.

What Is a General Ledger?

A general ledger is the master accounting record that contains all ledger accounts used to classify and summarize financial transactions for a business. The general ledger organizes every financial transaction into specific account categories defined by the chart of accounts. The chart of accounts is a structured listing of all ledger accounts, including assets, liabilities, equity, revenue, and expense accounts, used within an accounting system.

The general ledger maintains up-to-date account balances for each ledger account by receiving posted journal entries from the general journal. Account balances in the general ledger reflect the cumulative effect of all financial transactions recorded during an accounting period. The general ledger provides the data needed to prepare financial statements such as the balance sheet, income statement, and cash flow statement.

The general ledger plays 3 critical roles in accounting:

- Consolidating all financial transactions into categorized ledger accounts

- Maintaining accurate account balances for financial reporting

- Serving as the primary source for preparing the trial balance report and financial statements

Modern accounting software automates the general ledger by linking journal entries directly to ledger accounts, reducing manual errors and increasing the speed of financial reporting. Accounts payable software and spend management platforms integrate with the general ledger to track liabilities, invoice processing, and cash flow management in real time.

What Is a General Journal?

A general journal is the chronological record where all financial transactions are first recorded as journal entries using debit and credit format. The general journal functions as the “book of original entry” in a double-entry accounting system. Every financial transaction enters the accounting system through the general journal before the posting process transfers the journal entries to the general ledger.

Journal entries in the general journal record 4 essential elements for each financial transaction:

- The date of the financial transaction

- The names of the accounts affected

- The monetary amounts for each debit and credit

- A brief narration describing the financial transaction

The general journal ensures that every financial transaction maintains the fundamental rule of double-entry accounting: total debits must equal total credits. The general journal captures financial transactions that do not fit into specialized journals, including adjusting entries, closing entries, depreciation entries, and interest income or interest expense entries.

Recording financial transactions in the general journal provides a complete audit trail of all financial activity. The general journal supports accurate bookkeeping by preserving the chronological sequence of every financial transaction before the posting process distributes journal entries across the appropriate ledger accounts.

✓ Free initial consultation

What Is the Difference Between a General Ledger and a General Journal?

The general ledger organizes financial transactions by account, while the general journal records financial transactions in chronological order. The general ledger and the general journal differ in 5 key areas within the accounting cycle.

The 5 differences between a general ledger and a general journal are listed below:

- Purpose: The general journal records all financial transactions as journal entries in the order they occur. The general ledger classifies those journal entries into individual ledger accounts to maintain organized accounting records.

- Structure: The general journal uses a date-based, sequential format with debit and credit columns. The general ledger uses a T-account or columnar format organized by individual accounts from the chart of accounts.

- Position in the Accounting Cycle: The general journal comes first in the accounting cycle. The posting process transfers journal entries from the general journal to the general ledger.

- Level of Detail: The general journal contains the full narrative and debit and credit breakdown for each financial transaction. The general ledger shows summarized account-level data and running account balances.

- Role in Financial Reporting: The general ledger is the primary source for preparing financial statements and the trial balance report. The general journal serves as the supporting documentation and audit trail for all accounting records.

The general journal and general ledger are both essential components of a double-entry accounting system. Neither replaces the other; each serves a distinct function in maintaining accurate financial records.

What Is the Format of a General Ledger?

The general ledger follows a T-account or multi-column format, where each ledger account displays debits, credits, and a running balance. The format of the general ledger varies depending on the accounting system, manual or digital, but 5 standard elements appear in every general ledger format.

The 5 standard elements of the general ledger format are listed below:

| Element | Description |

|---|---|

| Account Name | The name of the ledger account (e.g., Cash, Accounts Payable, Revenue) |

| Accounnt Number | A unique code from the chart of accounts is assigned to each ledger account |

| Date | The date the journal entry was posted from the general journal |

| Debit Column | The debit amount posted to the ledger account |

| Credit Column | The credit amount posted to the ledger account |

| Balance | The running balance of the ledger account after each posted entry |

Modern accounting software displays the general ledger in a columnar format with automated balance calculations. The general ledger format supports financial reporting by enabling accountants to review account balances, trace posted journal entries, and prepare financial statements such as the balance sheet and income statement.

What Is the Format of a General Journal?

The general journal uses a tabular format, which includes date, account name, description, debit, and credit. The format of the general journal is designed to capture complete debit and credit details for every financial transaction in chronological order.

The 5 standard columns of the general journal format are listed below:

| Column | Purpose |

|---|---|

| Date | Records the date of the financial transaction |

| Account Title | Lists the accounts debited and credited |

| Description/Narration | Provides a brief explanation of the financial transaction |

| Debit (Dr.) | Records the debit amount for the transaction |

| Credit (Cr.) | Records the credit amount for the transaction |

The debit account is listed first, followed by the credit account (indented) in traditional journal entry format. The general journal format requires that the total debit amount equals the total credit amount for every journal entry, maintaining the integrity of double-entry accounting.

Accounting software and eInvoicing platforms automate the general journal by generating journal entries from financial transactions such as invoice processing, accounts payable, and revenue recognition, reducing manual data entry errors in bookkeeping.

How Do the General Ledger and General Journal Work in Accounting?

The general journal and general ledger work together through the posting process, where journal entries move from the general journal into categorized ledger accounts in the general ledger. The relationship between the general journal and the general ledger forms the backbone of the accounting cycle in a double-entry accounting system.

The general journal and general ledger function through 5 sequential steps in the accounting cycle:

- Identifying the financial transaction: Every financial transaction (sale, purchase, expense, or adjustment) is identified and documented with source records.

- Recording journal entries in the general journal: The financial transaction is recorded in the general journal with the appropriate debit and credit amounts.

- Posting journal entries to the general ledger: The posting process transfers each journal entry from the general journal to the corresponding ledger accounts in the general ledger.

- Updating account balances in the general ledger: The general ledger updates the running balance for each affected ledger account after every posted journal entry.

- Preparing financial statements from the general ledger: Account balances from the general ledger are used to generate the trial balance report, balance sheet, income statement, and cash flow statement.

The accounting system relies on the general journal for chronological accuracy and the general ledger for account-level accuracy. Accounting software streamlines the posting process by automatically transferring journal entries from the general journal to the general ledger, eliminating manual posting errors.

Spend management and accounts payable software further enhance the accounting cycle by automating invoice processing, categorizing expenses into the correct ledger accounts, and maintaining real-time visibility into financial activity and cash flow management.

✓ Free initial consultation

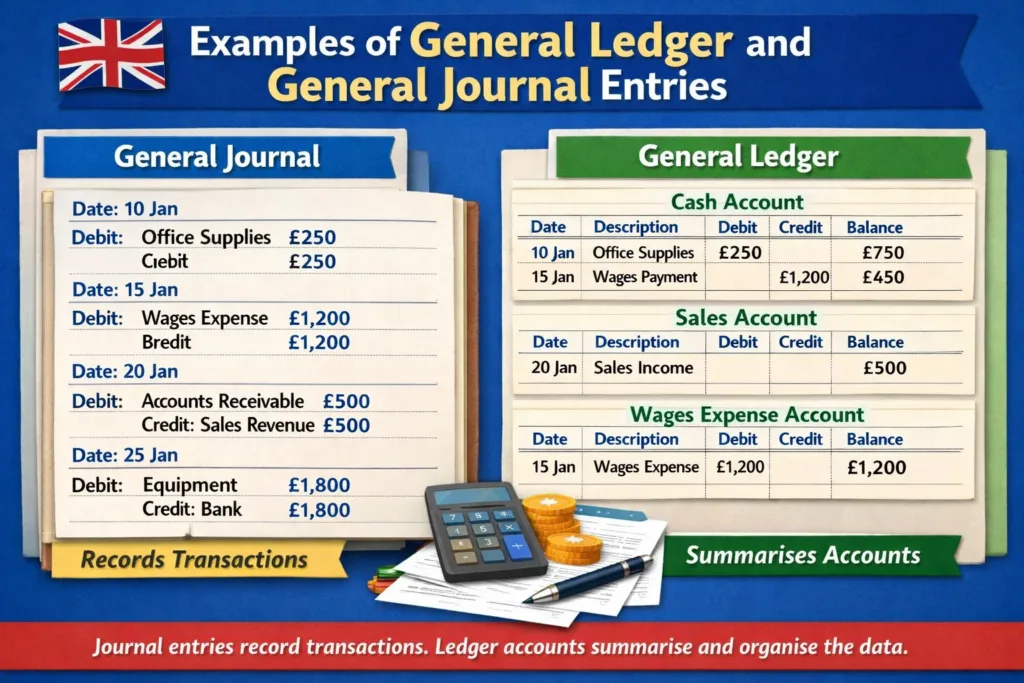

What Are Examples of General Ledger and General Journal Entries?

General journal entries record specific financial transactions with debit and credit amounts, and the posting process transfers those entries to the corresponding ledger accounts in the general ledger.

What Is the Role of the General Ledger and the General Journal in Double-Entry Accounting?

The general ledger and the general journal are the 2 foundational records of a double-entry accounting system, ensuring every financial transaction is recorded with equal debits and credits. Double-entry accounting requires that every financial transaction affect at least 2 accounts, one debited and one credited, to maintain the accounting equation: Assets = Liabilities + Equity.

The general journal serves as the entry point where every financial transaction is first recorded using a debit and credit format. The general ledger serves as the classification system where those journal entries are organized into ledger accounts that feed directly into financial statements.

The double-entry accounting system relies on the general journal and general ledger to accomplish 3 objectives:

- Maintaining the accounting equation (Assets = Liabilities + Equity) across all financial transactions

- Providing a complete, traceable record of every financial transaction through journal entries and ledger postings

- Enabling the preparation of accurate financial statements, including the balance sheet, income statement, and cash flow statement

The general journal and general ledger together form the core of bookkeeping and financial reporting. Accounting software automates the double-entry accounting system by linking journal entries in the general journal directly to ledger accounts in the general ledger.

How Are Debit and Credit Entries Recorded in Double-Entry Accounting?

Debit and credit entries are recorded in double-entry accounting by debiting one account and crediting another account for equal amounts in every financial transaction. Debits increase asset and expense accounts and decrease liability, equity, and revenue accounts. Credits increase liability, equity, and revenue accounts and decrease asset and expense accounts.

Every journal entry in the general journal must have equal total debits and total credits. The posting process transfers these debit and credit entries from the general journal to the corresponding ledger accounts in the general ledger. The trial balance report verifies that total debits equal total credits across all account balances in the general ledger.

Are the General Ledger and General Journal the Same?

No, the general ledger and the general journal are not the same. The general ledger and the general journal serve 2 different functions in the accounting cycle. The general journal is the book of original entry where all financial transactions are recorded chronologically as journal entries. The general ledger is the book of final entry where journal entries are classified and posted into individual ledger accounts.

The general journal captures the full debit and credit details of every financial transaction. The general ledger summarizes those transactions by account category and maintains running account balances. The general journal and the general ledger work together, but each serves a unique purpose in maintaining accurate accounting records and producing reliable financial statements.

Which Comes First: General Ledger or General Journal?

The general journal comes first in the accounting cycle. Every financial transaction is recorded in the general journal as a journal entry before the posting process transfers the entry to the general ledger. The sequence in the accounting cycle follows this path:

financial transaction → general journal (journal entry) → posting process → general ledger (ledger account).

The general journal must precede the general ledger because the general ledger depends on journal entries from the general journal to update account balances. Reversing this sequence would produce inaccurate accounting records and unreliable financial reporting.

Which Is More Important: the General Ledger or the General Journal?

The general ledger and the general journal are equally important in a double-entry accounting system. The general journal provides a detailed, chronological record of all financial transactions, while the general ledger provides the organized, account-level summary needed for financial reporting. Removing either record would break the accounting cycle.

The general ledger is more directly used for preparing financial statements such as the balance sheet, income statement, and cash flow statement. The general journal is more directly used for auditing, tracing individual financial transactions, and verifying the accuracy of journal entries.

What Is the Difference Between a General Ledger and a Trial Balance?

The general ledger contains all ledger accounts with their full transaction history, while the trial balance is a summary report listing all account balances from the general ledger at a specific date. The trial balance report verifies that total debits equal total credits across the general ledger.

The 3 key differences between a general ledger and a trial balance are listed below:

- Scope: The general ledger contains every posted journal entry and the full transaction history for each ledger account. The trial balance report lists only the closing account balances.

- Purpose: The general ledger serves as the complete financial record for the business. The trial balance serves as a verification tool to detect posting errors.

- Timing: The general ledger is maintained continuously throughout the accounting period. The trial balance report is prepared at the end of the accounting period before generating financial statements.

The trial balance report is derived from the general ledger. An imbalanced trial balance, where total debits do not equal total credits, indicates errors in the posting process from the general journal to the general ledger.

What Is the Difference Between a General Ledger and a Subsidiary Ledger?

The general ledger contains summarized account balances, and a subsidiary ledger contains the detailed individual records that support a specific general ledger account. A subsidiary ledger breaks down a control account in the general ledger into individual sub-accounts.

The 2 most common subsidiary ledgers in accounting are listed below:

- Accounts Receivable Subsidiary Ledger: Contains individual customer account balances that collectively equal the Accounts Receivable control account in the general ledger.

- Accounts Payable Subsidiary Ledger: Contains individual vendor account balances that collectively equal the Accounts Payable control account in the general ledger.

The total balance of all sub-accounts in a subsidiary ledger must equal the balance of the corresponding control account in the general ledger. Subsidiary ledgers provide detailed financial records for accounts payable and accounts receivable without cluttering the general ledger. Accounts payable software and spend management platforms use subsidiary ledgers to track individual vendor invoices through invoice processing and eInvoicing workflows.

What Is the Difference Between a General Ledger and a Journal Entry?

The general ledger is an accounting record containing all ledger accounts, while a journal entry is a single recorded financial transaction in the general journal. A journal entry is the smallest unit of recording in the accounting system. The general ledger is the comprehensive collection of all ledger accounts that receive posted journal entries.

The relationship between a general ledger and a journal entry works as follows:

A journal entry records a financial transaction in the general journal → the posting process transfers the journal entry to the appropriate ledger account → the general ledger updates the account balance for that ledger account.

How the General Ledger Supports Tax Filing and Compliance

The general ledger supports tax filing and compliance by providing a complete, categorized record of all financial transactions needed to calculate taxable income, deductible expenses, and tax liabilities. Tax authorities require businesses to maintain accurate financial records, and the general ledger serves as the primary source of those financial records.

Accounting software automates general ledger reporting for tax compliance by categorizing financial transactions, calculating depreciation schedules, and generating pre-formatted financial statements for submission to tax authorities.

How VAT Transactions Are Recorded in the General Ledger

Value-Added Tax (VAT) transactions are recorded in the general ledger through dedicated VAT ledger accounts that track VAT collected on sales (Output VAT) and VAT paid on purchases (Input VAT). The difference between Output VAT and Input VAT determines the net VAT liability or refund owed by the business.

VAT transactions in the general ledger involve 3 account types:

- Output VAT (VAT Payable): Records the VAT amount charged to customers on sales. Output VAT is a liability account in the general ledger.

- Input VAT (VAT Receivable): Records the VAT amount paid to suppliers on purchases. Input VAT is an asset account in the general ledger.

- VAT Settlement Account: Records the net VAT payable or receivable after offsetting Output VAT against Input VAT at the end of the VAT reporting period.

The general ledger posting increases Accounts Receivable by $11,500 (debit), increases Revenue by $10,000 (credit), and increases Output VAT by $1,500 (credit).

eInvoicing platforms and accounting software automate VAT recording in the general ledger by calculating VAT amounts from invoice processing data, posting journal entries to the correct VAT ledger accounts, and generating VAT return reports for compliance filing. Accurate VAT recording in the general ledger ensures compliance with tax regulations and prevents errors in VAT filings.

✓ Free initial consultation