The accounting equation is the foundational formula in accounting. It states that a company’s assets are always equal to its liabilities plus its equity. Every financial transaction a business records must keep this equation balanced.

The main benefit of the accounting equation is that it gives an instant snapshot of a business’s financial position. It shows what a business owns, what it owes, and what is left over for the owner. This makes it the backbone of the double-entry bookkeeping system and the balance sheet.

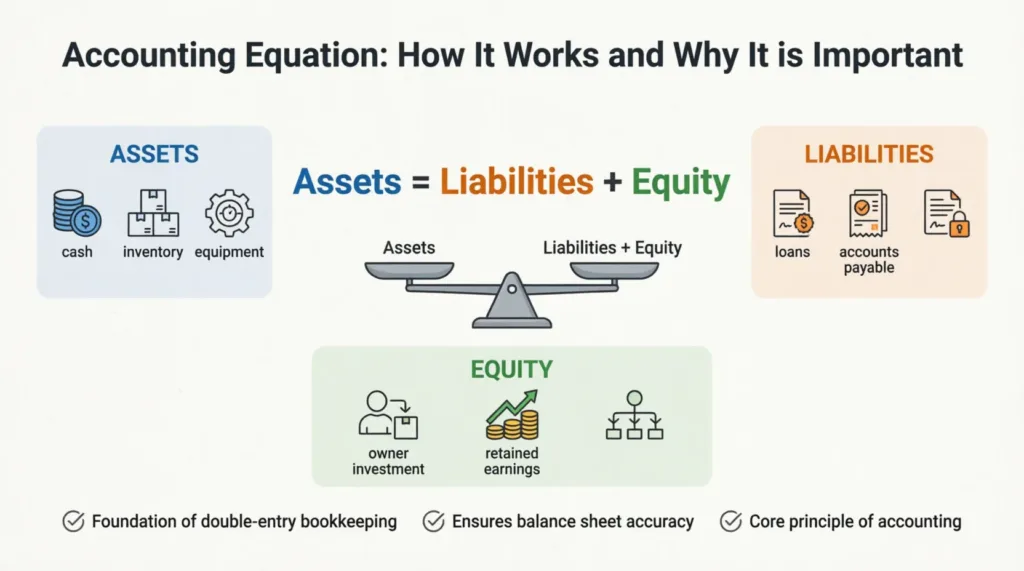

What is the Accounting Equation?

The accounting equation is a core principle in financial accounting that states a company’s total assets are equal to the sum of its total liabilities and its equity. The basic accounting equation formula is:

Assets = Liabilities + Equity

The accounting equation is also called the balance sheet equation or the fundamental accounting equation. It ensures that every financial transaction recorded in a company’s books keeps the balance sheet balanced.

The accounting equation captures the relationship between what a business controls (assets), what it owes (liabilities), and what the owner is entitled to (equity). A change in one element always results in an equal change in another, which is why this relationship is described as an accounting identity.

What is the Accounting Equation Formula?

The accounting equation formula is:

Assets = Liabilities + Equity

This can also be expressed in two alternative forms:

Equity = Assets – Liabilities

Liabilities = Assets – Equity

All three expressions describe the same relationship. The most common version is Assets = Liabilities + Equity because it mirrors the layout of a balance sheet, where assets appear on one side and liabilities plus equity appear on the other.

Here is a worked example using GBP figures. A business has:

- Equipment worth £15,000

- Inventory worth £16,000

- Cash in the bank of £20,000

- Money owed by customers (accounts receivable) of £24,000

Total assets: £75,000

The business owes:

- £37,000 in long-term loans

- £7,000 in taxes

- £6,000 in unpaid bills

Total liabilities: £50,000

£75,000 (Assets) – £50,000 (Liabilities) = £25,000 (Equity)

The book value (equity) of this business is £25,000. This is what the owner would be left with after selling all assets and paying off all debts.

What are the Elements of the accounting equation?

The accounting equation has 3 elements: assets, liabilities, and equity. Each element plays a distinct role in describing a business’s financial position.

- Assets are everything a business owns or controls that has economic value.

- Liabilities are every debt and financial obligation the business must pay.

- Equity is the net worth of the business, calculated as assets minus liabilities.

These three elements are directly reflected in the balance sheet. The left side of a balance sheet shows assets. The right side shows liabilities and equity. The two sides must always be equal, which is why the equation is called the balance sheet equation.

How Does the Accounting Equation Work?

The accounting equation works by recording every business transaction as at least two entries in the accounting system. This is known as double-entry bookkeeping. For every debit entry, there is a corresponding credit entry of equal value.

Take a practical example. A business takes out a bank loan of £50,000. This increases the business’s cash (an asset) by £50,000 and simultaneously increases its loan liability by £50,000. The equation stays balanced:

Assets (+£50,000 cash) = Liabilities (+£50,000 loan) + Equity (unchanged)

Now, say the business uses £25,000 of that cash to buy equipment. Cash decreases by £25,000, and equipment increases by £25,000. Total assets stay the same. The equation remains balanced.

Every transaction, whether it is buying inventory, paying wages, issuing equity shares to investors, or collecting money from customers, follows the same pattern. The accounting equation gives a running check that every entry in the books is correctly recorded.

Why is the Accounting Equation Important?

The accounting equation is important because it is the structural foundation of all financial accounting. It keeps the balance sheet balanced, ensures every transaction is recorded twice, and provides a quick check on the accuracy of financial records.

The accounting equation also gives insight into the financial health of a business. When equity is positive, the business owns more than it owes. When the accounting equation gives a negative equity result, the business is insolvent, meaning it could not pay its debts even if it liquidated all its assets.

Lenders use the equation to assess solvency before approving loans. Investors use it to evaluate the net worth of a business and its capital structure. Accountants use it to verify that financial statements produced under GAAP or IFRS are accurate and complete.

Who uses the Accounting Equation?

Four main groups that use the accounting equation are accountants, business owners, investors, and lenders. Accountants use the accounting equation to verify that every transaction is correctly recorded and that the balance sheet remains in balance. It is a daily tool for maintaining accurate books.

Business owners use the accounting equation to understand their net worth, monitor their financial position, and track whether the business is growing or taking on too much debt. Investors use the accounting equation to evaluate equity and assess the book value of a business before making investment decisions.

Lenders use the accounting equation to determine whether a business has enough assets to cover its liabilities before approving credit or long-term loans. Tools like Xero use the accounting equation automatically. Every transaction entered into cloud accounting software updates assets, liabilities, and equity in real time, keeping the balance sheet balanced without manual calculation.

What is the Expanded Accounting Equation?

The expanded accounting equation breaks equity down into its individual components. The basic equation treats equity as a single figure. The expanded version shows where equity comes from:

Assets = Liabilities + Owner’s Capital + Revenue – Expenses – Drawings

In corporate accounting, this becomes:

Assets = Liabilities + Share Capital + Retained Earnings + Revenue – Expenses – Dividends

The expanded accounting equation is useful for understanding how day-to-day business activity, such as generating revenue or paying expenses, affects the equity balance. It connects the income statement to the balance sheet and gives a more detailed picture of how equity changes over an accounting period.

What is an Asset in the Accounting Equation?

An asset in the accounting equation is any resource owned or controlled by a business that has economic value and is expected to provide a future benefit. Assets are recorded on the left side of a balance sheet.

Assets fall into two main categories. Tangible assets include cash, accounts receivable, inventory, equipment, vehicles, buildings, and property. Intangible assets include licenses, copyrights, trademarks, patents, and other forms of intellectual property.

Assets are also classified by liquidity. Liquid assets, such as cash and accounts receivable, can quickly be converted into cash. Fixed assets, such as machinery and buildings, are held for many years and are less liquid.

What is a Liability in the Accounting Equation?

A liability in the accounting equation is any debt or financial obligation the business owes to an external party. Liabilities are recorded on the right side of a balance sheet, alongside equity.

Liabilities include unpaid bills, overdrafts, credit cards, long-term loans, mortgages, accounts payable, deferred revenue, holiday pay owed to workers, and tax liabilities that have not yet been paid. Both short-term and long-term debts count as liabilities.

Adding liabilities reduces equity. Paying down liabilities increases equity. This relationship is central to understanding how a business manages its debt and financial leverage.

What is Equity in the Accounting Equation?

Equity in the accounting equation is the net worth of the business. Equity is calculated as total assets minus total liabilities. It represents what the owner or shareholders would receive if the business sold all its assets and paid off all its debts.

Equity increases when a business generates profit or when owners contribute additional capital. Equity decreases when a business reports a loss or when owners withdraw funds (drawings or dividends).

The book value of a business is another way of expressing equity. It reflects the accounting value of the business based on recorded assets and liabilities, rather than market value.

What is Shareholders’ Equity in the Accounting Equation?

Shareholders’ equity is the total value of the company that belongs to its shareholders. It is the amount that would remain if the company liquidated all its assets and paid off all its liabilities, with the remainder distributed to shareholders.

Shareholders’ equity includes share capital (money raised by issuing equity shares to investors), retained earnings (cumulative profits not paid out as dividends), and other reserves. Retained earnings represent profits that have been saved and reinvested into the business rather than distributed to shareholders.

What is the Formula for Total Equity?

The formula for total equity is:

Total Equity = Total Assets – Total Liabilities

For a sole trader or partnership, this is called owner’s equity or net worth. For a corporation, it is called shareholders’ equity or stockholders’ equity. The calculation is the same in both cases.

For example, if a business has total assets of £75,000 and total liabilities of £50,000, total equity is £25,000. This £25,000 represents the book value that the owner retains after all debts are settled.

What is the Purpose of the double-entry bookkeeping system?

The purpose of the double-entry bookkeeping system is to record every financial transaction in at least two accounts, ensuring the accounting equation stays balanced at all times.

In a double-entry system, every transaction has a debit side and a credit side. Debits and credits must always be equal. This means every change to an asset, liability, or equity account is matched by an equal and opposite change elsewhere in the records.

The double-entry bookkeeping system was developed to prevent errors and fraud. Because every transaction affects two or more accounts, any mistake creates an imbalance in the equation, making it easier to detect. This system is the basis for all modern financial accounting and is required under GAAP and IFRS reporting standards.

How Does the Accounting Equation Help Businesses?

The accounting equation helps businesses in 4 key ways.

- Financial accuracy: The equation acts as a built-in error check. If the balance sheet does not balance, there is a recording error that must be found and corrected.

- Transaction analysis: The equation shows how each transaction affects the financial position of the business, helping owners and managers understand the impact of spending and investment decisions.

- Solvency monitoring: By tracking equity over time, businesses can see whether they are growing their net worth or eroding it through excessive debt or losses.

- Reporting compliance: The accounting equation underpins financial statements produced under accounting standards, including GAAP and IFRS. Keeping the equation balanced ensures financial statements are accurate and compliant.

What is the Difference Between the Accounting Equation and the Balance Sheet?

The accounting equation and the balance sheet describe the same financial relationship, but in different formats. The accounting equation is a formula: Assets = Liabilities + Equity. It is a concise mathematical expression of a company’s financial position.

The balance sheet is a formal financial statement that presents this same information in detail, listing every individual asset, liability, and equity account. The balance sheet shows the full picture: cash balances, accounts receivable, inventory, fixed assets, loans, tax liabilities, share capital, and retained earnings.

The accounting equation is the rule that keeps the balance sheet balanced. Every line on the balance sheet must conform to the equation. This is why the balance sheet is also called the statement of financial position.

What Are the Limitations of the Accounting Equation?

The accounting equation has 3 main limitations.

- It does not measure performance. A balanced equation only confirms that records are mathematically consistent, not that the business is profitable or well-managed.

- It relies on historical cost. Assets are recorded at their original purchase price, not their current market value. This means the book value of a business can differ significantly from its actual market value.

- The equation cannot account for the quality of management, brand strength, and customer loyalty, all of which affect the real value of a business. The accounting equation does not capture qualitative factors.

Investors and analysts use the accounting equation alongside other financial ratios and statements, including the income statement and the cash flow statement, to build a complete picture of a business’s financial health.

How Can Accounting Help My Business Grow?

Accounting helps a business grow by providing accurate financial data that supports better decision-making. With clear records of assets, liabilities, equity, revenue, and expenses, business owners can identify where money is being made, where it is being lost, and where investment will generate the best return.

Accurate accounting also improves access to finance. Lenders and investors require financial statements that conform to accounting standards before providing funding. A business with well-maintained accounts is in a stronger position to secure loans or attract investment.

Using cloud accounting software like Xero automates much of the record-keeping, reduces the risk of error, and gives business owners real-time visibility of their financial position. This makes it easier to plan, budget, and grow with confidence.

Why Do I Need a Professional Bookkeeper?

A professional bookkeeper ensures that every transaction is recorded correctly, that the accounting equation stays balanced, and that financial statements are accurate and ready for tax reporting.

Bookkeeping errors can lead to misstated accounts, incorrect tax returns, and poor business decisions based on unreliable data. A professional bookkeeper catches these errors before they cause problems.

A bookkeeper also keeps records organised according to accounting standards, which is important if a business is ever audited or needs to present accounts to lenders or investors. For small business owners without an accounting background, a professional bookkeeper provides the expertise needed to keep the books in order and comply with financial regulations.

Businesses can find qualified bookkeeping and accounting professionals through an advisor directory. Platforms like Xero also connect business owners with certified advisors who have experience with cloud accounting and can provide ongoing support.