The accounting cycle is the ongoing process businesses use to track and record financial transactions throughout an accounting period. This process makes sure that all activity is captured, classified, and shown in the financial statements.

The steps of the accounting cycle involve identifying transactions, recording journal entries, posting to the general ledger, preparing a trial balance, making adjusting entries, preparing an adjusted trial balance, creating financial statements, and closing the books.

The accounting cycle is important because it provides reliable financial statements, supports informed decision-making, helps monitor a business’s financial health, and maintains compliance with reporting standards. It also makes the business’s financial information trustworthy for stakeholders.

The purpose of the accounting cycle is to transform individual financial transactions into accurate, complete financial statements that show a business’s performance over an accounting period. It confirms reliable financial information for reporting, decision-making, and compliance with standards by organising and processing accounting records in a consistent way.

What Is the Accounting Cycle?

The accounting cycle is the complete, repeating sequence of steps that a business follows to identify, record, and report every financial transaction that occurs within a given accounting period. It helps transform raw economic activity into reliable, auditable financial statements.

This cycle is based on the principles of double-entry bookkeeping to make sure that every transaction is recorded in a balanced way with corresponding debits and credits. The accounting cycle provides a consistent structure for recording transactions and organising financial data so that businesses can maintain reliable, standardised financial records.

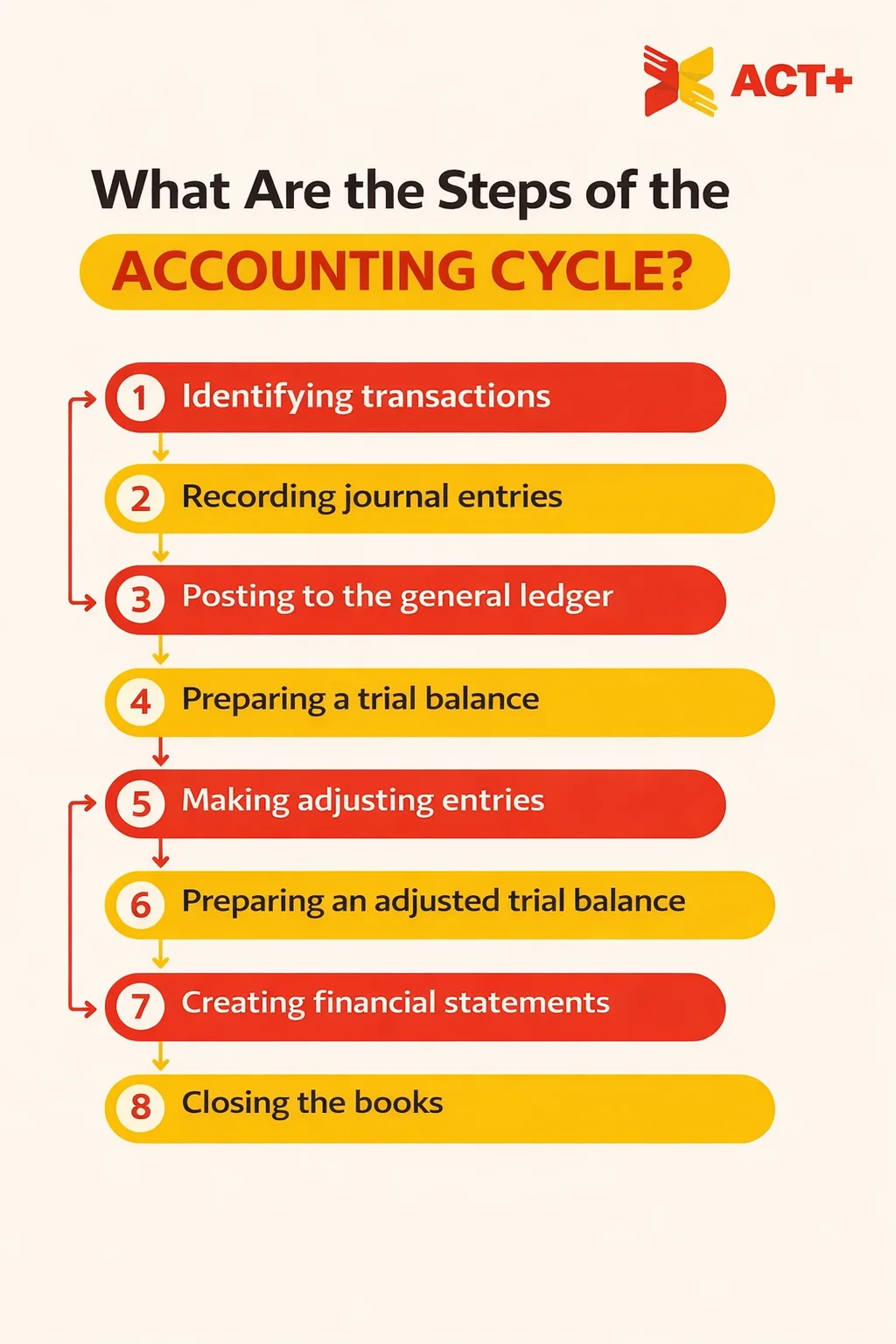

What Are the Steps of the Accounting Cycle?

The steps of the accounting cycle are identifying transactions, recording journal entries, posting to the general ledger, preparing a trial balance, making adjusting entries, preparing an adjusted trial balance, creating financial statements, and closing the books.

Here are the 8 steps of the accounting cycle are listed below.

- Identify transactions: Each accounting cycle starts when a financial event that has an accounting impact occurs in a business. The initial task of the accountant is to identify that the event occurred and collect its documentation, like an invoice, a receipt, a purchase order, a bank record, or a contract. No record of entry is made without evidence. This step determines which raw material will pass through the remaining processes of the cycle.

- Record journal entries: A transaction after identification is posted to the general journal in chronological order. Every single journal entry includes a date, the accounts that are impacted, the amounts, and a short description. All entries should have at least one debit and one credit of equal value with the principles of double-entry bookkeeping, and the accounting equation should be in balance at the very time a transaction is recorded.

- Post to the general ledger: The journal entries are then moved or posted to the general ledger, which is a master record that puts all the transactions together by account. The ledger also has a running balance in each account in the T-account format. Posting groups the raw journal entries into categories, such as cash, accounts receivable, sales revenue, or rent expense, and it is now possible to observe the cumulative activity of any account and balance at any point in time.

- Prepare a trial balance: The balance of all ledger accounts at the end of the accounting period is brought to a trial balance to verify that total debits and total credits are equal. It acts as a checking tool, and the differences should be rectified before going ahead.

- Make adjusting entries: Ledger balances do not always show the actual financial position at the end of the period, and therefore, accrual accounting is used to make adjustments (recognise revenues when earned and expenses when incurred). Some of the common adjustments are accruals, deferrals, prepayments, and depreciation, which make financial statements correct.

- Preparing an adjusted trial balance: All adjustments are recorded, and the adjusted trial balance is prepared with updated account balances. It makes sure that the books are correct and are applied in the compilation of financial statements. It is important to correct any mistakes before proceeding.

- Create financial statements: The adjusted trial balance is used to prepare the three main financial statements, which include the income statement (to calculate net income), the statement of retained earnings (to update equity), and the balance sheet (to show assets, liabilities, and equity). These statements are the final goal of the accounting cycle.

- Close the books: Closing entries finalise the accounting cycle by transferring balances from temporary accounts (revenues, expenses, and dividends) to retained earnings and resetting these accounts to zero. Permanent accounts (assets, liabilities, equity) remain open and carry their balances into the next period. The cycle restarts after closing entries and preparing a post-closing trial balance while making sure the ledger is accurate.

✓ Free initial consultation

Why Is the Accounting Cycle Important?

The accounting cycle is important because it is the framework of proper financial reporting. It provides completeness, consistency, and traceability of accounting records by making sure that all the transactions are run through the same disciplined process from identification to closing. Mistakes go unnoticed, statements become incomparable, and the figures relied on by managers and other stakeholders are no longer reliable.

The checkpoints built into the cycle serve as a flexible error-detecting mechanism that identifies misclassifications and omissions before the financial statements. Its repeatable nature makes it easier to identify anomalies and prevent fraud, since there should be an auditable record of transactions.

What is the purpose of the accounting cycle?

The purpose of the accounting cycle is to make sure that all the financial transactions that a business conducts are recorded, categorised, and reported correctly in each accounting period. It uses the rules of double-entry bookkeeping to make the accounting equation balance throughout the entire amount of activity that a business generates, thereby causing its accounting records to become complete, traceable, and subject to review.

The cycle offers a consistent and trustworthy foundation for all stakeholders, which includes management, investors, lenders, and regulators, who rely on the company’s financial information to make informed decisions. Its recurrent form also generates an uninterrupted, similar record over time, such that a business can evaluate improvement, see patterns, and hold itself accountable over time. The cycle does not just close the books at period-end but makes the numbers relevant enough that all the individuals who depend upon them operate with confidence.

What Is the Role of the Accounting Cycle in Auditing?

The role of the accounting cycle in auditing is to provide an audit trail, support substantive testing, help evaluate internal controls, improve error detection, support fraud identification, and validate financial statement preparation.

The role of the accounting cycle in auditing is outlined below.

- Provides an audit trail: Every activity in the accounting cycle, such as source documentation to journal entries, ledger entries, and trial balance, is an audit trail. Auditors track the figures in financial statements back to the source transaction and make sure they are accurate and authentic.

- Supports substantive testing: Substantive testing is based on proper accounting documentation. Proper compliance with the accounting cycle helps the auditors effectively test the transactions and balances. A lack in the accounting cycle makes the testing process more costly and time-consuming.

- Helps evaluate internal controls: The accounting cycle serves as a financial reporting control system. The auditors evaluate its procedures, which include the trial balances, approvals, and reconciliations, to make sure that errors are avoided or identified and the extent to which they can trust the accounting records of the company.

- Improves error detection: Checking processes in the accounting cycle, such as trial balances, are used to identify errors and misclassifications before they are released to financial statements. The cycle needs to be well-maintained to confirm that mistakes are reduced and any complications are identified and fixed with ease, which reduces the chances of misstatements.

- Supports fraud identification: The double-entry system of the accounting cycle is what makes every transaction match and traceable, and thus it is difficult to hide fraud. Abnormal entries or variances that cannot be explained are revealed during auditing, and this assists in identifying fraud.

- Validates financial statement preparation: The accounting cycle is used to implement accounting standards, which include recording accruals, deferrals, and depreciation, matching revenues and expenses, and closing accounts. An auditor verifies step by step that a cycle is correctly completed, which indicates compliance.

✓ Free initial consultation

How Does the Accounting Cycle Make Auditing Easier?

The accounting cycle makes auditing easier by creating a clear, sequential record that connects every figure in the financial statements back to its originating journal entries. The trial balance gives auditors a single, verified starting point, which reduces the time spent tracing errors. It also allows auditors to focus their testing on material risks rather than basic reconciliation work.

How Does the Accounting Cycle Help a Small Business?

The accounting cycle helps a small business by providing a structured process for recording every transaction. It produces accurate financial statements and maintains a clear view of financial health each period. Combined with accounting software, it reduces manual errors and makes sure the business stays organised, tax-ready, and equipped to make confident financial decisions.

What Is the Difference Between the Accounting Cycle and the Budget Cycle?

The accounting cycle is the ongoing process businesses use to track and record financial transactions throughout an accounting period. This process makes sure all activity is captured, classified, and shown in the financial statements. The budget cycle looks forward, planning expected revenues and expenses across a fiscal year.

What Is the Difference Between the Accounting Cycle and the Operating Cycle?

The accounting cycle is a bookkeeping process that records and reports all financial transactions within a fixed period. The operating cycle is a business process that measures the time between purchasing inventory and collecting cash through accounts receivable.

How Long Does the Accounting Cycle Take to Complete?

The duration of the accounting cycle depends on the accounting period a business follows, which can be monthly, quarterly, or annually. Most companies complete the cycle at the end of a fiscal year, when they close the books and prepare financial statements. Shorter cycles occur for internal reporting or regulatory requirements, but the full process maintains accuracy and compliance.

Who Is Responsible for Performing the Accounting Cycle?

The accounting cycle is performed by accountants or bookkeepers, who handle recording transactions and maintain accurate financial records. They sometimes use accounting software to simplify the process, but the responsibility lies with trained personnel. They make sure all steps, from journal entries to financial statement preparation, are completed accurately and in compliance with accounting standards.

Who Are the Users of the Accounting Cycle?

The users of the accounting cycle include business owners, managers, and accountants who rely on accurate financial statements for decision-making and financial reporting. Auditors use the cycle to verify records during auditing. Investors, creditors, and small businesses also depend on its outputs to assess financial performance and make informed economic decisions.

What Are the Limitations of the Accounting Cycle?

The limitations of the accounting cycle are its reliance on historical costs instead of current market values. The process is time-consuming, costly, and subject to human error or manipulation, offering a backwards-looking view rather than predicting future performance.

How Do You Design an Accounting Cycle for Your Business?

To design an accounting cycle for your business, start by defining your accounting period and setting up a chart of accounts to organise financial activities. Collect all source documents for transactions and choose appropriate accounting software to record, classify, and summarise them. This structured approach offers accurate financial tracking and reporting.

How Do Accounting Services Handle the Accounting Cycle for You?

Accounting services handle the accounting cycle for you from recording transactions to preparing adjusting entries and closing entries. They organise accounts, reconcile balances, and produce accurate financial statements and reports. Accounting services in the UK confirm timely and reliable financial reporting while reducing the risk of errors and compliance issues by handling these tasks.

Can Online Bookkeeping Services Make the Accounting Cycle Faster?

Yes, online bookkeeping services make the accounting cycle faster by automating the recording of transactions and organising financial transactions using advanced accounting software. These online bookkeeping services reduce manual work, minimise errors, and allow real-time updates. Such services make the process more reliable and help businesses maintain accurate accounts with less time and effort.

✓ Free initial consultation