Accounting is the systematic process of recording, classifying, and reporting financial transactions, such as sales revenue, equipment purchases, and salary payments. This helps a business understand its financial position and make informed decisions about budgeting, investing, and managing expenses. It is built on the fundamental accounting equation, Assets = Liabilities + Equity, because this equation shows how a company’s resources are financed through borrowing or owner investment. Accounting uses the Double-Entry Bookkeeping system so that every transaction affects two accounts, such as recording cash received from a sale as a debit to cash and a credit to sales revenue. Ensuring the records remain balanced.

Accounting plays a vital role in tracking income, expenses, assets, and liabilities while producing key financial reports such as the balance sheet, income statement, and cash flow statement. These reports help business owners, investors, and regulators evaluate financial performance, maintain transparency, and comply with established standards like Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS).

The field of accounting includes several specialized areas such as Financial Accounting, Managerial Accounting, Tax Accounting, Auditing, and Forensic Accounting. These branches support different functions, from external financial reporting to internal business analysis and fraud detection.

What Is Accounting?

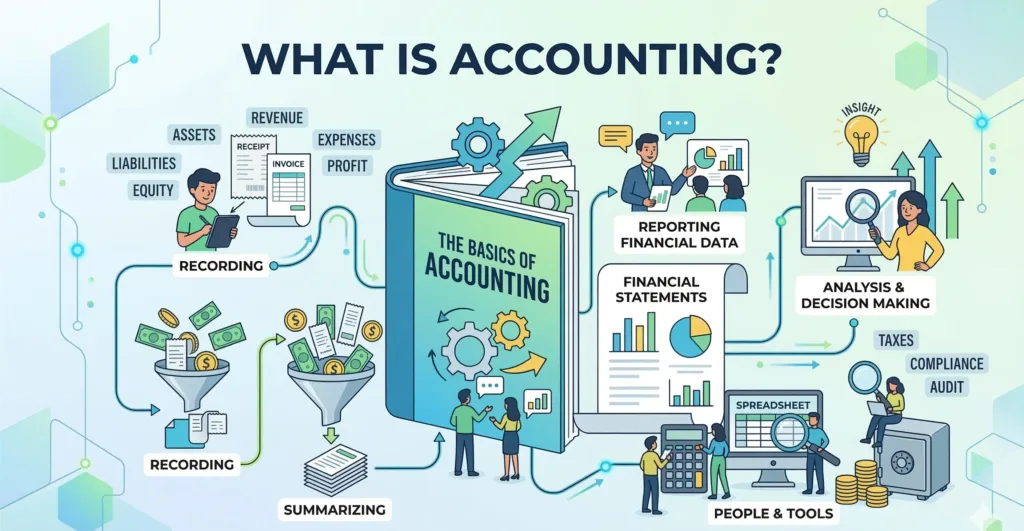

Accounting is the systematic process of identifying, recording, classifying, and communicating financial information about a business or organization. It tracks every financial transaction, income earned, expenses paid, debts owed, and assets owned, and organizes that data into reports used for decision-making.

The core accounting equation states: Assets = Liabilities + Equity. This equation is the foundation of the double-entry bookkeeping system, where every transaction affects at least two accounts, one debit and one credit, keeping the equation in balance.

What is the Purpose of Accounting?

The purpose of accounting is to provide accurate, timely financial information that supports decision-making, ensures legal compliance, and measures business performance. There are 5 core purposes:

- Recording transactions: Every financial event is documented in journals and ledgers.

- Summarizing data: Raw transactions are condensed into financial statements, the balance sheet, income statement, and cash flow statement.

- Communicating results: Financial reports are shared with investors, creditors, tax authorities, and management.

- Ensuring compliance: Accounting keeps businesses aligned with tax laws, GAAP, or IFRS reporting requirements.

- Supporting planning: Historical financial data informs budgets, forecasts, and strategic resource allocation.

✓ Free initial consultation

Why Accounting Is Important?

Because it gives businesses the financial narrative needed to grow, stay compliant, and attract funding. Without accounting, a business cannot track whether it is profitable or identify which products generate the most revenue.

There are 6 specific reasons accounting matters:

- Business growth: Accounting reveals which products sell and which departments drag profits down, enabling smarter investment decisions.

- Funding access: Investors and banks require audited financial statements before providing capital or loans.

- Owner exit planning: When selling a business, its valuation is based on financial records prepared through accounting.

- Managing payments: Accounting tracks which vendors are owed money and when payments are due, protecting supplier relationships.

- Collecting receivables: Businesses that extend trade credit track outstanding invoices through accounts receivable records.

- Legal compliance: Public companies must file financial statements under GAAP or IFRS. Failure to comply results in fines or delisting from stock exchanges.

What is an example of Accounting?

The example of accounting is the double-entry method applied to a customer invoice. When a business sends an invoice to a client for $5,000, the accountant records a debit to accounts receivable (an asset) for $5,000 and a credit to sales revenue for $5,000. This entry flows into both the balance sheet and the income statement.

When the client pays the invoice, the accountant records a second entry: a debit to cash for $5,000 and a credit to accounts receivable for $5,000. The net result is that cash increases and the receivable is cleared, the books remain balanced.

Another example involves inventory. A business buys $2,000 of inventory on credit. Under accrual accounting, the accountant records a debit to inventory (asset) for $2,000 and a credit to accounts payable (liability) for $2,000 immediately when the purchase is made. When payment is sent 30 days later, a debit to accounts payable and a credit to cash close out the transaction.

What Are Accounting Basics?

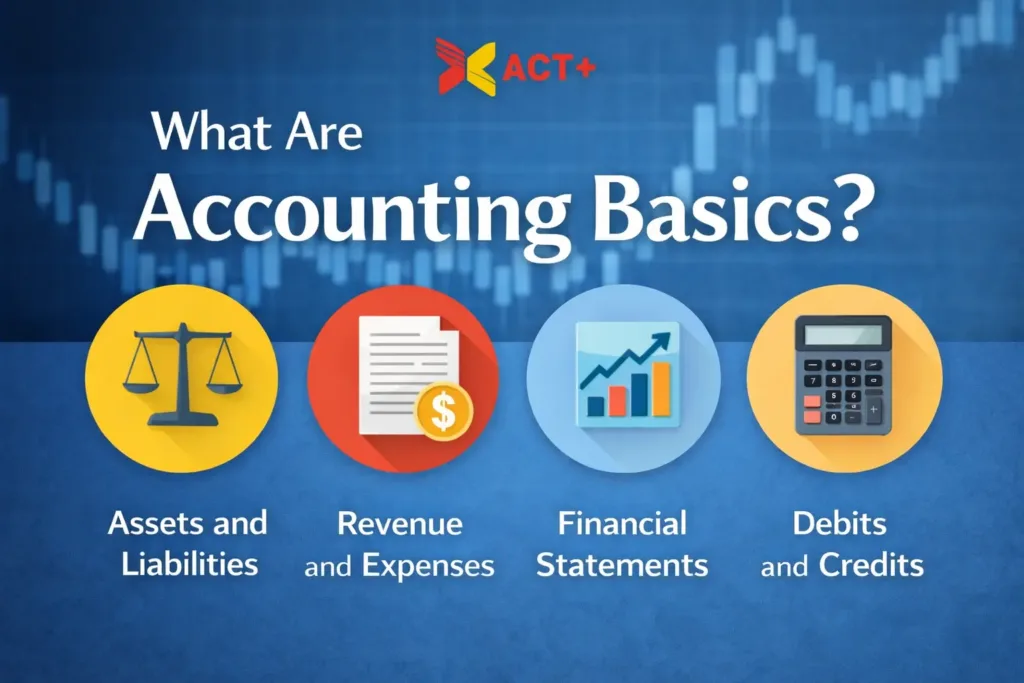

Accounting basics rest on a set of core concepts that define how financial data is categorized and measured. The 7 fundamental accounting basics are:

- Accounting Equation: Assets = Liabilities + Equity. This equation must always balance, and every transaction is recorded to maintain that balance.

- Assets: Resources owned by a business with measurable economic value, including current assets (cash, accounts receivable, inventory) and noncurrent assets (property, equipment, patents).

- Liabilities: Obligations the business owes to others, such as loans, accounts payable, and accrued expenses.

- Equity: The residual interest in assets after liabilities are deducted. For corporations, this is shareholders’ equity.

- Revenue: Income generated from primary business activities, such as product sales or service fees.

- Expenses: Costs incurred to generate revenue, including wages, rent, utilities, and materials.

- Double-entry bookkeeping: Every transaction affects at least two accounts, a debit entry and a credit entry, ensuring the accounting equation stays balanced. A debit increases assets or expenses and decreases liabilities or equity. A credit does the opposite.

Financial statements are built from these components. The balance sheet reports assets, liabilities, and equity at a point in time. The income statement shows revenue minus expenses to arrive at net profit or loss. The cash flow statement shows how cash moved in and out of the business.

What is the History of Accounting?

The history of accounting spans thousands of years, beginning in ancient Mesopotamia, Egypt, and Babylon, where merchants and governments kept records of grain, livestock, and taxes. Ancient Rome maintained detailed public financial records, an early form of government accounting.

The Father of Accounting is Luca Pacioli, an Italian mathematician who published a landmark book in 1494 describing the double-entry system of bookkeeping. Pacioli documented the method Venetian merchants used to track assets, liabilities, and equity across two matched entries, the same method still used today.

Modern accounting as a formal profession emerged in the 19th century. By 1880, the Institute of Chartered Accountants in England and Wales was established, largely driven by the needs of industrialization. Merchants and factory owners needed reliable financial records as businesses grew more complex and bankruptcy risks increased.

In the 20th century, accounting became more standardized. The Financial Accounting Standards Board (FASB) was established in the United States, producing the Generally Accepted Accounting Principles (GAAP). Internationally, the International Accounting Standards Board (IASB) developed the International Financial Reporting Standards (IFRS), now used in over 140 countries.

In 2019, the Alliance for Responsible Professional Licensing (ARPL) was formed in the U.S. to defend rigorous standards for Certified Public Accountant (CPA) certification against proposals to lower qualification requirements.

What are the Different Types of Accounting?

There are 7 main types of accounting, each serving a different function within a business or organization.

Forensic Accounting

Forensic accounting investigates financial fraud, embezzlement, and other financial crimes. Forensic accountants analyze records, trace transactions, and build evidence for legal proceedings. Forensic fraud detection work is used in litigation support, insurance claims, divorce proceedings, and regulatory investigations.

Auditing

Auditing is the independent examination of financial statements to verify accuracy and compliance. Internal auditors work inside organizations to assess controls and risk. External auditors, typically from CPA firms, conduct annual audits required by law for public companies and by lenders as part of debt covenants.

Financial Accounting

Financial accounting produces the external financial statements, the balance sheet, income statement, and cash flow statement, which summarize a company’s performance over a reporting period. These reports follow GAAP in the United States or IFRS internationally. Most large companies have their financial statements audited annually by an external Certified Public Accountant (CPA) firm. Companies traded on public stock exchanges are legally required to produce audited financial statements.

Tax Accounting

Tax accounting manages a company’s tax obligations under federal, state, and local law. Tax accountants use different rules from financial accountants, following the Internal Revenue Code (IRC) in the United States. Their work includes filing compliance, strategic tax planning to minimize liabilities, and overseeing the entire tax lifecycle of an organization, from entity structure setup to return filing and remittance.

Cost Accounting

Cost accounting focuses on the costs of producing goods or services. It tracks direct costs like raw materials and labor, indirect costs like overhead, and fixed vs. variable costs. Manufacturers use cost accounting to set product prices, evaluate production efficiency, and control expenses. In cost accounting, money is treated as an economic factor of production, not just a performance measure.

Fund Accounting

Fund accounting is a specialized accounting system used mainly by non-profit organizations and governments to track resources according to their intended purpose, focusing on accountability rather than profitability. It ensures that funds provided by donors, grants, or laws are used exactly as designated.

Managerial Accounting

Managerial accounting uses financial data to support internal decision-making. Unlike financial accounting, which produces standardized external reports, managerial accounting generates monthly or quarterly reports tailored to management needs. These reports cover budgeting, forecasting, variance analysis, and operational efficiency. Managerial accountants help executives decide where to cut costs, where to invest, and how to allocate resources across departments.

✓ Free initial consultation

What is the Accounting Cycle?

The accounting cycle is a structured sequence of activities that begins when a financial transaction occurs and ends when the books are closed for that period.

It repeats every fiscal period (monthly, quarterly, annually) to provide updated financial information. The accounting cycle is the 6-step process that converts raw financial transactions into complete, accurate financial statements.

- Collect transaction data: Gather invoices, bank statements, receipts, payment requests, and other source documents that record business activity.

- Post journal entries: Record each transaction as a debit and credit entry in the general journal, then transfer to the appropriate general ledger accounts.

- Prepare an unadjusted trial balance: Pull all general ledger balances to confirm that total debits equal total credits. This step catches entry errors before adjustments.

- Post adjusting journal entries: At the end of the period, record accruals, deferrals, and corrections to reflect actual financial activity not yet captured.

- Prepare the adjusted trial balance: Run the trial balance again after adjustments to confirm everything is accurate before producing statements.

- Prepare financial statements: Use the adjusted trial balance to produce the income statement, balance sheet, and cash flow statement for the period. Then record closing entries to reset revenue and expense accounts to zero for the new period.

The chart of accounts (COA) is the organized list of all accounts used in this cycle. Every journal entry references a specific account, asset, liability, equity, revenue, or expense from the COA.

What Are Accounting Standards?

Accounting standards are the rules that govern how financial transactions are recorded and reported. They ensure comparability, consistency, and transparency across organizations and industries. The 2 dominant accounting standards frameworks are GAAP and IFRS.

Generally Accepted Accounting Principles (GAAP) is the standard used in the United States, maintained by the Financial Accounting Standards Board (FASB). GAAP is rules-based, meaning it provides detailed, specific guidance for many types of transactions. U.S. public companies must follow GAAP for all financial reporting.

International Financial Reporting Standards (IFRS) is used in over 140 countries, governed by the International Accounting Standards Board (IASB). IFRS is principles-based, giving companies more judgment in applying the standards. The European Union, Canada, Australia, and most of Asia follow IFRS.

What Does the Accountant Do?

An accountant records, analyzes, and reports financial information for businesses, governments, and individuals. Accountants ensure that financial records are accurate, compliant with applicable standards, and useful for decision-making. Basic accounting tasks can be handled by a bookkeeper. For complex tax, audit, or advisory work, a qualified accountant.

What are the responsibilities of an accountant?

An accountant has six core responsibilities:

- Recording daily financial transactions in the general ledger using the double-entry system.

- Preparing financial statements, the balance sheet, income statement, and cash flow statement, at the end of each reporting period.

- Reconciling accounts against bank statements, vendor invoices, and other external documents.

- Filing tax returns and managing tax compliance for the organization.

- Conducting or supporting internal and external audits.

- Providing financial analysis and advisory services to management for budgeting and planning.

What are the different types of accounting careers?

There are 6 common accounting career paths:

- Auditor (internal or external): Reviews financial records for accuracy and compliance. External auditors work for CPA firms; internal auditors work within companies.

- Tax accountant: Manages tax planning, compliance, and filing. Works to minimize tax liabilities while staying within the law.

- Forensic accountant: Investigates financial fraud and irregularities, often for legal cases or regulatory inquiries.

- Managerial accountant: Analyzes financial data and advises management on cost control, budgets, and operational decisions.

- Controller: Oversees the accounting department, managing financial reporting, accounts payable, accounts receivable, and procurement.

- IT/Systems accountant: Manages the accounting information system (AIS), ensuring financial software and data integrity.

What skills are required for accounting?

Accounting requires five skill areas:

- Attention to detail: Accountants must catch subtle errors in transaction records, reconciliations, and financial statements.

- Analytical thinking: Reviewing financial data to identify trends, anomalies, and areas for improvement requires structured logical reasoning.

- Mathematical competency: Basic arithmetic and understanding of percentages, ratios, and financial metrics are required, though modern software handles most calculations.

- Knowledge of accounting standards: Familiarity with GAAP, IFRS, or the IRC is required, depending on the role and industry.

- Technology proficiency: Accountants use accounting information systems (AIS), spreadsheet tools, and specialized accounting software daily.

What is the difference Between Accounting and Bookkeeping?

The key difference is that bookkeeping focuses on recording daily financial transactions. Accounting involves interpreting, analyzing, and reporting those records to guide decision-making.

A bookkeeper records what happens. An accountant explains what it means and what to do about it. Bookkeepers typically do not require formal licensing, while accountants often hold designations like CPA or CMA. For simple transactional work, a bookkeeper is sufficient. For audits, tax strategy, or financial analysis, a qualified accountant is required.

Is accounting worth it for a small business?

Yes, accounting is worth it for a small business. Proper accounting helps a small business track cash flow, prepare accurate tax returns, qualify for loans, and understand profitability. Without accounting records, small business owners cannot identify which products or services generate the most profit or where costs are out of control.

A small business that maintains clean accounting records also builds credibility with lenders and investors, making it easier to access financing for growth.

What are the accounting tips for small businesses?

There are 6 practical accounting tips for small businesses:

- Separate personal and business finances by opening a dedicated business bank account from day one.

- Record transactions weekly rather than waiting until tax season to avoid missing entries and losing receipts.

- Track accounts receivable carefully to ensure customers pay on time and cash flow stays healthy.

- Reconcile bank accounts monthly to catch errors, unauthorized charges, or missing transactions early.

- Set aside a percentage of every revenue payment for taxes to avoid a large unexpected bill at year-end.

- Use accounting software to automate invoicing, expense tracking, and financial report generation.

How to do accounting for a small business?

To do accounting for a small business, follow these 5 steps:

- Choose an accounting method: Cash accounting records transactions when money changes hands. Accrual accounting records revenue when earned and expenses when incurred, regardless of payment timing. Most small businesses start with cash accounting for simplicity, but accrual accounting gives a more accurate picture of long-term financial health.

- Set up a chart of accounts (COA): Create categories for all assets, liabilities, equity, revenue, and expenses relevant to the business.

- Record all transactions: Log every sale, purchase, and payment using debits and credits in a journal, then post to the general ledger.

- Reconcile accounts monthly: Compare ledger balances against bank and credit card statements to catch errors.

- Produce financial statements quarterly: Generate the income statement, balance sheet, and cash flow statement to monitor financial performance and prepare for tax filings.

What is the best accounting software for small businesses?

The best accounting software for small businesses includes QuickBooks, Xero, FreshBooks, Zoho Books, and Sage. QuickBooks is the most widely used in North America, offering invoicing, expense tracking, payroll, and tax preparation tools. Xero is popular for its cloud-based collaboration features. FreshBooks is designed for freelancers and service businesses. Sage suits small businesses that need more advanced inventory and manufacturing capabilities.

Larger businesses often use enterprise-grade solutions like Oracle NetSuite or SAP, which handle complex multi-entity reporting, consolidations, and integrations with other business systems.

What is the meaning of finance and accounting?

Finance refers to the management of money, investments, and capital, as well as decisions about where to allocate funds. And how to raise capital, and how to evaluate risk and return. Accounting refers to the recording, classification, and reporting of financial transactions.

Finance is forward-looking, focused on strategic resource allocation and investment decisions. Accounting is primarily backward-looking, producing accurate historical financial records.

What is an accounting information system?

An accounting information system (AIS) is the combination of people, processes, data, and technology that a business uses to collect, store, and process financial information. An AIS ranges from a simple spreadsheet to sophisticated enterprise software like Oracle or SAP.

What is the difference between accrual and cash accounting?

The difference between accrual and cash accounting lies in timing: cash accounting records income and expenses only when money changes hands, while accrual accounting records them when they are earned or incurred, regardless of actual cash flow.

For example, A business completes a $10,000 project in December but receives payment in January. Under accrual accounting, $10,000 in revenue is recorded in December. Under cash accounting, the $10,000 is recorded in January.

What is the difference between management accounting and financial accounting?

The difference between management accounting and financial accounting lies in their purposes and audiences. Management accounting focuses on providing detailed financial information to internal stakeholders. These stakeholders include managers and executives, who use this information to support strategic planning, operational control, and decision-making. Financial accounting is designed to prepare standardized financial statements for external stakeholders. This includes investors, creditors, regulators, and government authorities.