GAAP (Generally Accepted Accounting Principles) is the established accounting framework of accounting rules and principles that regulates how financial statements are prepared and presented. FASB (Financial Accounting Standards Board) is the independent body responsible for developing and maintaining those rules, particularly for public companies operating within the US financial reporting system.

offer in terms of role, scope, focus, revenue recognition, flexibility, leases, authority, and fair value measurement. Both serve the broader goal of reliable financial reporting, but they differ in nature. GAAP is the framework itself, the complete set of standards companies must follow. FASB is the institution behind it, continuously updating and refining those standards to show changing business realities.

Both GAAP and FASB matter, as GAAP delivers the accounting rules that ensure regulatory compliance, uniformity, investor confidence, and decision-making. FASB makes sure those rules remain authoritative, relevant, and aligned with the needs of public companies, investors, and regulators.

What is GAAP?

GAAP (Generally Accepted Accounting Principles) is a standardised set of accounting rules, requirements, and practices used by companies to compile their financial statements. These accounting standards make sure that financial reporting is transparent, consistent, and comparable across organisations.

What is FASB?

FASB (Financial Accounting Standards Board) is a private, non-profit, independent organisation responsible for establishing and improving financial accounting and reporting standards. FASB is an independent organisation, but it works closely with the SEC (Securities and Exchange Commission). The SEC sets accounting standards for public companies, but assigns the FASB for the private sector.

✓ Expert support for accounting & compliance

What is the Difference Between GAAP and FASB?

The difference between GAAP and FASB is in their roles, scope, focus, revenue recognition, flexibility, leases, authority, and fair value measurement.

| Features | GAAP | FASB |

|---|---|---|

| Role | A framework of accounting rules and principles | The standard-setting body that creates and updates GAAP standards |

| Scope | A complete set of financial reporting principles | Create and update standards |

| Focus | Confirms consistency, transparency, and comparability in financial reporting | Focuses on research, review, and issuance of new accounting guidance |

| Revenue Recognition | Applies the ASC 606 five-step model as the rule that entities must follow | Developed and issued ASC 606 as part of its standard-setting mandate |

| Flexibility | Provides the actual rules that entities must comply with | Developed and issued ASC 606 as part of its standard-setting mandate |

| Leases | Requires lessees to recognise most leases on the balance sheet under ASC 842 | Issued ASC 842 to modernise lease accounting and improve transparency |

| Authority | Recognised by the SEC as the accepted reporting framework | Private, independent body designated by the SEC to set GAAP |

| Fair Value Measurement | Applies ASC 820 as the standard for measuring and disclosing fair value | Developed ASC 820 to establish a single, consistent fair value framework |

Role

GAAP (Generally Accepted Accounting Principles) functions as the logical foundation. Its role is to provide the actual criteria, definitions, and methods that accountants use to confirm that financial statements are consistent and comparable. FASB (Financial Accounting Standards Board) functions as the administrative authority. Its role is to serve as the independent body that researches, develops, and updates the standards that define GAAP.

Scope

GAAP is comprehensive and instructional. It includes all finalised accounting rules and industry-specific requirements for sectors like healthcare, real estate, and banking. FASB is procedural and developmental. Its reach is limited to managing and updating the standards. FASB focuses on the due process of standard-setting rather than the daily application of those rules by businesses.

Focus

GAAP focuses on compliance and uniformity. Its main goal is to make sure that any two companies recording the same transaction do so in a way that allows an investor to compare them accurately. FASB focuses on transparency and relevance. Its goal is to identify accounting gaps or areas where current financial reporting fails to provide a clear understanding of economic reality. It creates new standards to meet those gaps.

Revenue Recognition

Revenue Recognition under GAAP follows the ASC 606 five-step model, which determines when income is considered earned and realisable. This standard applies universally across all entities and has been extended with industry-specific guidance. This industry-specific guidance makes sure complex contracts are accounted for consistently.

FASB evaluates and issues the updates to these requirements (such as the landmark ASC 606). It determines whether the revenue recognition rules need to change based on evolving business models, such as the shift from selling hardware to SaaS (Software-as-a-Service).

Flexibility

GAAP is generally restrictive, as it is a rules-based framework. It offers particular, often standard tests, with less scope for professional judgement than international standards. FASB represents the source of flexibility. It is an active board and has the power to issue practical alternatives or simplified transition methods so companies can be flexible in how they adopt complex new standards.

Leases

Most leases under GAAP must be recorded on the balance sheet as a right-of-use asset and corresponding liability under ASC 842. This liability means companies can no longer keep operating leases off-balance sheet. FASB introduced ASC 842 to replace the old standard and bring transparency to lease obligations. FASB gives investors a clear understanding of a company’s financial commitments.

Authority

GAAP holds its authority because the SEC formally recognises it as the accepted standard for financial reporting. FASB, a private and independent body, is specifically designated by the SEC to develop and maintain those GAAP standards.

Fair Value Measurement

ASC 820 under GAAP defines how assets and liabilities must be measured and shown at fair value. This principle defines the amount received in an orderly market transaction. FASB developed ASC 820 to replace disorganised guidance across different standards. FASB establishes one consistent framework that applies uniformly across all industries and asset types.

Why Are GAAP and FASB Important?

GAPP (Generally Accepted Accounting Principles) is important because it ensures regulatory compliance, uniformity, investor confidence, and decision-making. FASB (Financial Accounting Standards Board) is important, as it offers transparency, consistency, relevance, and market stability.

The reasons for GAAP’s importance are listed below.

- Regulatory compliance: GAAP is formally recognised by the SEC as the accepted reporting framework for public companies. Companies must follow GAAP to meet their legal obligations, avoid penalties, and maintain their standing with regulators. Companies risk delisting, fines, or legal action without compliance.

- Uniformity: GAAP requires all companies to follow the same accounting rules and principles when preparing financial statements. This uniformity confirms that every set of accounts is structured, presented, and reported consistently and predictably across all industries.

- Investor confidence: Financial statements prepared under GAAP are accurate, complete, and protected against fraud. This confidence is important for raising capital, as investors commit funds to companies whose financials are held to a recognised standard. Investors and analysts compare financials across different companies and industries on a similar basis.

- Decision-making: GAAP-compliant financial statements give management, investors, lenders, and regulators the reliable data they need to make informed financial decisions. The quality of the decision depends directly on the consistency of the financial information available, whether evaluating a merger, extending credit, or allocating resources.

The reasons for FASB’s importance are mentioned below.

- Transparency: FASB follows a due process before issuing any new accounting standard, which includes public consultations, exposure drafts, and stakeholder feedback. This open approach confirms that the standard-setting process is visible, well-reasoned, and accountable to all parties affected by financial reporting.

- Consistency: FASB develops and maintains a unified set of accounting standards that all entities are required to follow. This uniformity makes sure that financial statements are prepared on the same basis across all companies, sectors, and reporting periods. It also reduces variation and improves the reliability of reported figures.

- Relevance: FASB continuously reviews and updates accounting standards to show changes in business models, economic conditions, and financial instruments. It also makes sure the standards are relevant to real transactions and useful for stakeholders.

- Market stability: FASB contributes to the stability of capital markets by making sure that financial reporting is regulated by clear, consistent, and authoritative standards. It reduces unpredictability, prevents financial misrepresentation, and improves overall confidence in the integrity of financial markets.

✓ Expert support for accounting & compliance

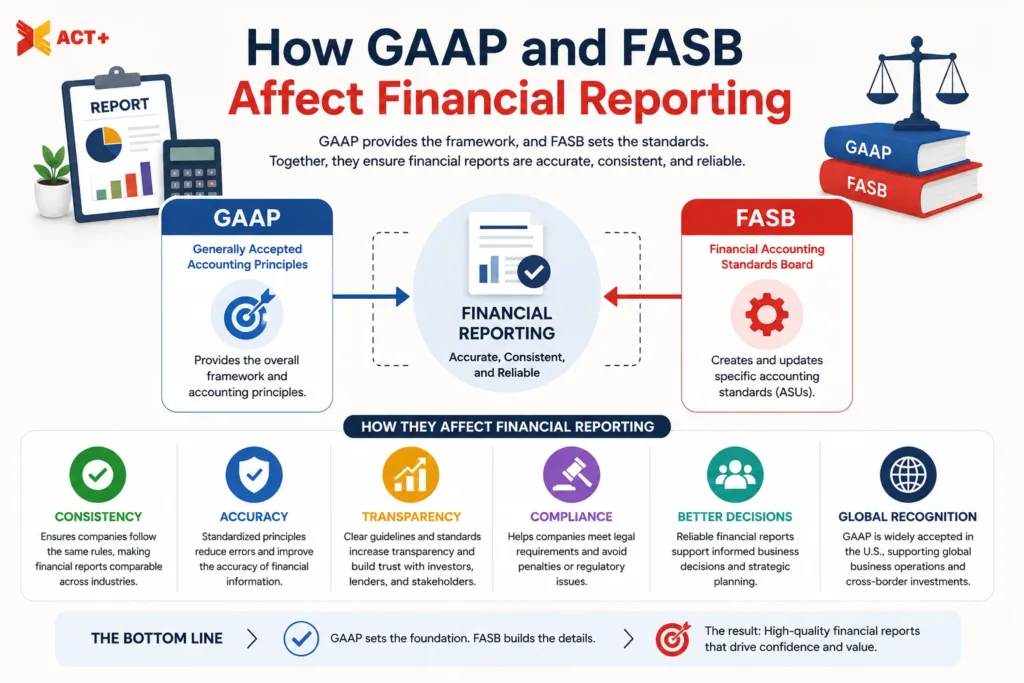

How Do GAAP and FASB Affect Financial Reporting?

GAAP and FASB affect financial reporting by standardising financial statements, balance sheet accuracy, revenue recognition in financial reporting, lease disclosure on the balance sheet, comparability across financial statements, and credibility and trust in financial reporting.

GAAP and FASB affect financial reporting in the listed ways below.

- Standardisation of financial statements: GAAP establishes the structure and content of all financial statements. It makes sure that the income statement, balance sheet, and cash flow statement are prepared uniformly across all entities. FASB supports this by issuing accurate standards that define how each aspect must be measured, recognised, and disclosed in financial reporting.

- Balance sheet accuracy: GAAP requires that all assets, liabilities, and equity on the balance sheet be recorded at fair values and according to defined GAAP rules. FASB standards, such as ASC 820 on fair value measurement, confirm that balance sheet figures show an accurate overview of a company’s financial position.

- Revenue recognition in financial reporting: GAAP mandates a strict five-step model under ASC 606 that determines when and how revenue is recognised in financial statements. FASB developed this standard to make sure that financial reporting across all industries shows the actual transfer of goods and services, rather than when cash is simply received.

- Lease disclosure on the balance sheet: ASC 842, under GAAP, requires most leases to be recorded directly on the balance sheet as a right-of-use asset and liability. FASB introduced this standard to improve transparency in financial reporting. It makes sure that lease obligations are fully visible to investors and stakeholders reviewing financial statements.

- Comparability across financial statements: GAAP makes sure that financial statements produced by different companies are comparable on a similar basis. FASB supports this by maintaining consistency in its standards. It allows investors and analysts to draw valid conclusions from financial reporting across different entities and sectors.

- Credibility and trust in financial reporting: GAAP gives financial statements regulatory credibility, as the SEC formally recognises it as the accepted framework for financial reporting. FASB affirms that GAAP is authoritative, current, and trustworthy for decision-making.

Can Companies Report Finances Without Following GAAP or FASB?

Private companies are not legally required to follow GAAP, as no federal law mandates it for non-public entities. Lenders, investors, and stakeholders usually demand GAAP-compliant financial statements before extending credit or capital. Public companies are legally obligated by the SEC to comply with GAAP in all financial reporting.

Are GAAP and FASB the Same?

No, GAAP and FASB are not the same. GAAP is the complete set of accounting standards and accounting rules that companies must follow in financial reporting. FASB is the independent body responsible for developing and maintaining those standards. FASB creates the accounting rules that form GAAP.

What Came First: GAAP or FASB?

GAAP came first. Basic accounting principles began to develop in the early 20th century, with GAAP gradually formalised following the 1929 stock market crash. FASB was not established until 1973. It was created to take over the responsibility of setting accounting standards from its predecessor bodies, under the direction of the SEC.

Who Created FASB and Why?

FASB was established in 1973 by the accounting profession to serve as an independent organisation responsible for standard-setting in the United States. The SEC formally recognised FASB as the authoritative body for developing accounting standards. FASB replaces predecessor bodies that were considered insufficiently independent and strict.

What Is the Role of the SEC in GAAP and FASB?

The SEC holds the legal authority to set accounting standards for public companies, but has transferred this responsibility to FASB. The SEC implements regulatory compliance by requiring all public companies to follow GAAP in their financial reporting. The SEC ensures that FASB-issued standards have the full scope of regulatory authority.

What Is the Difference Between GAAP and IFRS?

The difference between GAAP and IFRS (International Financial Reporting Standards) is that GAAP is a rules-based framework used in the US, developed by FASB, and IFRS is a principles-based set of international standards issued by the IASB. The two accounting standards differ in areas such as revenue recognition, inventory valuation, and lease accounting.

What Is the Difference Between FASB and IASB?

FASB is the US-based body responsible for standard-setting under GAAP, and the IASB develops IFRS, the globally adopted international standards used in over 140 countries. Both bodies collaborate on convergence projects, but their frameworks are different. The FASB is rules-based, while the IASB takes a broader, principles-based approach to standard-setting.

What Is the Difference Between FASB and GASB?

FASB is responsible for setting standards for private and public companies, and GASB (Governmental Accounting Standards Board) develops accounting standards specifically for state and local government entities. Both bodies operate independently, but they share a similar standard-setting structure, with GASB focused exclusively on government accounting reporting requirements.

What Is the Difference Between GAAP and GAAS?

GAAP is a framework of accounting rules that defines how financial statements are prepared and presented. GAAS (Generally Accepted Auditing Standards) governs how auditing is conducted when examining those statements. GAAP defines the accounting rules for reporting, and GAAS defines the auditing standards for verifying them.

Are GAAP and FASB Used Outside the US?

GAAP and FASB are primarily used within the US, governing US accounting practices for both public and private entities. Internationally, most countries have adopted IFRS as their preferred international standards. FASB collaborates with the IASB on convergence efforts to match US accounting standards more closely with IFRS.

Do Small Businesses Need to Follow GAAP?

Small businesses are not legally required to follow GAAP. Maintaining GAAP-compliant accounting records is strongly advisable, as lenders and investors expect proper financial accounting practices. Accounting compliance with GAAP also improves credibility, supports better decision-making, and prepares small businesses for future investment or growth opportunities.

What Are Common Mistakes About GAAP and FASB?

Common mistakes about GAAP and FASB are considering them as identical concepts and misunderstanding regulatory compliance as a requirement exclusive to large corporations. Another common mistake is viewing disclosure requirements and materiality thresholds as optional rather than mandatory.

Can Accounting Services Handle GAAP and FASB for You?

Yes, professional accounting services can manage accounting records, ensure regulatory compliance, and apply the correct financial accounting standards on a company’s behalf. These accounting services in the UK are important given the complexity of GAAP requirements for public companies. Legal responsibility for accurate and compliant reporting always remains with the company itself.

How Do Tax Services Help With GAAP and FASB Compliance?

Tax services support accounting compliance by making sure accounting records are maintained accurately and meet financial accounting standards. Tax services help with disclosure requirements, identify reporting gaps, and help companies meet regulatory compliance obligations under GAAP.

✓ Expert support for accounting & compliance